You can Download Chapter 4 Recording of Transactions II Questions and Answers, Notes, 1st PUC Accountancy Question Bank with Answers Karnataka State Board Solutions help you to revise complete Syllabus and score more marks in your examinations.

Karnataka 1st PUC Accountancy Question Bank Chapter 4 Recording of Transactions II

1st PUC Accountancy Recording of Transactions II One Mark Questions and Answers

Question 1.

What is journal proper?

Answer:

The journal proper is used for recording only those transactions which cannot be recorded in any of the other subsidiary books.

Question 2.

Mention any two transactions which recorded in journal proper.

Answer:

- Opening entries

- Closing entries

Question 3.

Write the opening entries meaning.

Answer:

When a newly business commenced, a trader record the assets liabilities brought in called opening entries.

Question 4.

What is closing entries in journal proper?

Answer:

At the end of accounting year all nominal a/c are transferred to trading and profit or Loss a/c, such transferring entries called closing entries.

Question 5.

What is transfer entry?

Answer:

Transfer entry is passed when an amount of one account is to be taken to some other account.

![]()

Question 6.

Give examples for closing entries.

Answer:

Example for transferring entries are, Building closing balance, closing stock etc.

- Transfer of total rent during the year to profit and loss a/c

- Transfer of total wages to trading account.

- Transfer of purchases by closing to trading account.

Question 7.

Write the entries for purchase return transfer to purchases.

Answer:

Purchase return a/c Dr.

To purchases account

Question 8.

What is cash book?

Answer:

Cash Book is a book of original entry book. It is a type of subsidiary book. It is maintained by business for recording cash receipts and payments during the year.

Question 9.

What is simple column cash book?

A cash book which contains only one amount colum called simple column cash book or single column cash book.

Question 10.

What is three – column cash book?

Three column cash book is a cash book which contains cash column, bank and discount column, there all cash bank & Discount related transactions are recorded.

Question 11.

What is two column cash book?

The cash book which contains of discount column and cash column called two column cash book or cash book with cash and discount.

![]()

Question 12.

What are contra entries?

A single transaction entering both the side of three calumn cash book called contra entries.

Question 13.

What is cash discount?

Cash discount is an allowances or deductions made from the amount due. It is allowed by creditor to debtors

Question 14.

What is trade discount?

Trade discount is a reduction in the catalogue price or invoice price of the goods sold.

Question 15.

Write the specimen of single column cash book.

Answer:

Question 16.

Write the specimen of double column cash book.

Answer:

Question 17.

Write the specimen of triple column cash book or cash book with Discount and bank.

Answer:

Question 18.

Give two examples for contra entries.

Answer:

Example for contra entries are :

- Cash deposted into bank

- Cash withdraw for office use.

![]()

Question 19.

How do you treat cash received 9000 in full settlement against amount due of X 10000.

Answer:

An amount received Rs. 9000 recorded in cash column and Rs. 1000 recorded in discount column on debit side of double /Triple column cash book.

Question 20.

Why cash account will always show a debit balance.

Answer:

Generaly we can spend equivatent to reciept or less than that because of this cash always have debit balance or tallied both the side of cash book.

Question 21.

Define subsidiary books.

Answer:

Subsidiary book may be defined as ‘The books of original entry containing a specialised and homogeneous class of transcations maintained daily in a chronological order’. It is also called special journals.

Question 22.

Write any three features of subsidiary books.

Answer:

Features of subsidiaiy books are :

- It is a book of original entry of transactions. They substitute the journal.

- Each subsidiary books contains specialised transations having common characterstics.

- Entering transactions is simple and much earlier than journalising.

Question 23.

Mention any four types subsidiary books.

Answer:

Usual subsidiary books are :

- Purchase book

- Sales book

- Purchase return book

- Sales return book

- Bills receivable

- Bills payable

- Cash book

- Journal proper

![]()

Question 24.

What is purchase book?

Answer:

It is a type of subsidiary book which contains all details of credit purchase of goods during the year.

Question 25.

What is an invoice?

Ans.

Invoice or bills is a statement of goods along with quantity and price which is issued by seller to purchases.

Question 26.

What is meant by purchase return book or return outwards?

Answer:

It is a type of subsidiary books. It contains the details of goods return to supplier.

Question 27.

What is the cash discount?

Answer:

It is an allowance given by creditor to the debtor for prompt payment of the debt.

Question 28.

Write the meaning of debit note.

Answer:

It is a statement containing the details of the goods returned as a quntity, rate, etc. The returner will prepare this note.

Question 29.

What is sales book?

Answer:

It is a type of subsidiary book or special ledger. Where all credit sales of goods recorded in a set of original book of entry called sales book.

Question 30.

What is sales return book?

Answer:

It is a type of subsidiary books. In this book all returns from debtors and allowance granted are recorded. It is also called as return inward books.

![]()

Question 31.

Write the meaning of credit note.

Answer:

It is a statement containing the details of goods returned as quantity, rates etc. The credit note is prepared by the receiver of goods.

Question 32.

Write any two similarities between purchase and sales book.

Answer:

- Both purchase and sales book records credit transactions.

- Both records only transactions related to goods.

Question 33.

Differentiate sales book and purchase book.

Answer:

Question 34.

Write any two advantages of subsidiary books.

Answer:

- Division of work possible and upto date accounts is possible with the help of subsidiary books.

- There will be considerable savings of labour time.

Question 35.

What is trade discount?

Answer:

It is an allowance or reduction from the catalogue price or invoice price of goods allowed by saler to customer.

Question 36.

What is discount?

Answer:

Discount means reduction or deduction in the invoice price or invoice price of goods or on the amount of debt payable.

![]()

Question 37.

Write the difference between cash and trade discount.

Answer:

Question 38.

Write any two differences between subsidiary books and ledger.

Answer:

Question 39.

Differentiate debit note and credit note.

Answer:

Question 40.

Write two circumstances of debit note preparation.

Answer:

- When goods are returned to supplir.

- When any allowances claim from supplir.

1st PUC Accountancy Recording of Transactions II Additional Questions and Answers

Question 1.

Briefly state how the cash book is both journal and a ledger?

Answer:

Transactions are recorded directly form the source of documents in the Cash Book, so there is no need to record transactions in the Journal book. Further, on the basis of the cash transactions recorded in the Cash Book, cash and bank balances can be determined and so there is no need to prepare cash account (which is a part of ledger) separately. Thus, the Cash Book serves the purpose of both Journal as well as ledger. .

Question 2.

What is the purpose of contra entry?

Answer:

Contra entry represents deposits or withdrawals of cash form bank or vice versa. The purpose of contra entry is to indicate the transactions that effect both cash and bank balances. This entry does not affect the financial positions of a business. A contra entry is recorded in both sides of receipts of payments of Cash Book and is denoted by ’C’ in the ledger folio column.

Question 3.

What are special purpose books?

Answer:

Business transactions are large in number and difficult to record; so, journal is sub-divided for quick, efficient and accurate recording of the business transactions. Special purpose books like, sales book and purchases book are maintained for those transactions that are routine and repetitive in nature.

![]()

Question 4.

What is petty cash book? How it is prepared?

Answer:

Petty Cash Book is used for recording payment of petty expenses, which are of smaller denominations like postage, stationary, conveyance, refreshment, etc. person who maintains petty cash book is known as petty cashier and these small expenses are termed as petty expenses.

It is prepared by two methods:

Ordinary system: In this case, a fixed sum of money is paid to petty cashier for the payment of petty expenses and after spending the whole amount, the account is submitted by the petty • cashier to the main cashier.

Imprest system: In this case, a fixed sum of the money is given to the petty cashier in the beginning of a period and at the end of the period the amount spent by him is reimbursed, so that he has a fixed amount in the beginning of every new period.

Question 5.

Give the meaning of posting of journal entries.

Answer:

Posting is the process of transferring the business transactions form Journal to ledgers. Every transaction is first recorded in the journal and subsequently transferred to their respective accounts.

Question 6.

Mention the purpose of maintaining subsidiary journal.

Answer:

The process of accounting starts from identification of financial and non-financial events. Financial events are first recorded in a Journal. A small business has lesser number of transactions and thereby it may be possible to record these transactions through Journal entry. However, on the contrary, as the business grows, there will be voluminous number of transactions and the firm may experience difficulty, thereby it becomes tedious to record through Journal entry. Thus, in order to save time and effort, it is recommended to sub divided Journal.

The purpose of maintaining subsidiary Journal are given below.

- It saves time and efforts in recording.

- It enables division of work, leading to an enhancement of efficiency and effectiveness, as particular accountant takes care of particular books.

- It also makes each accountant more responsible and accountable for the books assigned to them.

- It records routine and repetitive transactions at one place, which leads to easy accessibility of information and hassle-free communication.

Question 7.

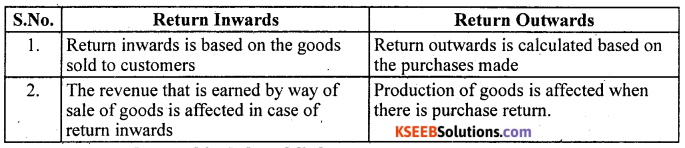

Write the difference between return inwards and return outwards.

Answer:

Question 8.

What do you understand by ledger folio?

Answer:

Ledger folio is a page number of an account in ledger that is written in the L.F. column of a journal format. In journal entry, ledger folio number is written corresponding to the name of the account in the L.F. column. It helps in easy locating of the account in the ledger book. It reduces the time in recording and rechecking.

![]()

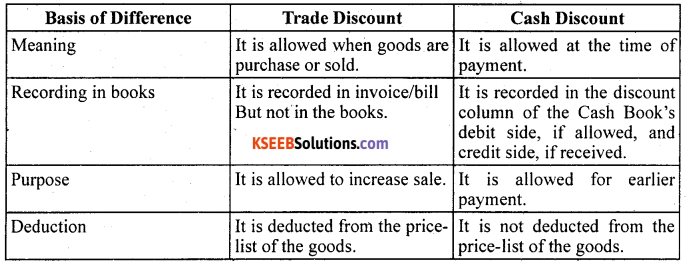

Question 9.

What is the difference between trade discount and cash discounts?

Answer:

Question 10.

Write the process of preparing ledger form a journal

Answer:

The process of preparing ledger from Journal can be explained with the help of an example. Let us suppose that machinery is purchased from Mr. X, so, the journal entry will be: Machinery A/c Dr

To Mr. X Account

In this example, Machinery Account is debited and Mr. X Account is credited. Let us understand the process of preparing ledger from the journal entry.

Account which is debited in the entry:

Step 1: Identity the account in ledger that is debited, i.e., ‘Machinery Account’.

Step 2: Enter date in the debit side of the ‘Machinery Account’ in the ‘Date column.

Step 3: Enter the name of the account as ‘Mr. X Account’ (which is credited in the entry) in the ‘Particulars’ column in the debit side of the Machinery Account.

Step 4: Enter the page number of the journal, where the entry is recorded in the ‘ J.F’. (Journal folio) column. ‘

Step 5: Post the corresponding amount in the ‘Amount’ column, which is recorded against ‘Machinery Account’ in the journal entry.

Account which is credited in entry:

Step 1: Identify the account in ledger that is credited, i.e., ‘Mr. X Account’.

Step 2: Enter date in the credit side of ‘Mr. X Account’ in the ‘Date’ column.

Step 3: Enter the name of the account as ‘Machinery Account’ (which is debited in the entry) in the ‘Particulars’ column in the credit side of the ‘Machinery Account’.

Step 4: Enter the page number of the journal where the entry is recorded in the ‘J.F’. (journal folio) column.

Step 5: Post the corresponding amount in the ‘Amount’ column, which is recorded against ‘Mr. X Account’in the journal entry.

Question 11.

What do you understand by Imprest amount in petty cash book?

Answer:

Imprest amount is an amount of money given by the main cashier to the petty cashier in the beginning of a period. At the end of the period, the amount spent by the petty cashier gets reimbursed in such a manner, that he has the same amount qf cash in hand in the beginning of next period.

1st PUC Accountancy Recording of Transactions II Six Marks Questions and Answers

Long Answers

Question 1.

Explain the need for drawing up the special purpose books.

Answer:

The needs for drawing up the special purpose book are given below:

- Quick and efficient recording: It is a time consuming process to record all the transactions in a journal. If there are separate books, then recording of transactions can be done more efficiently and timely. So, the need of special purpose book arises.

- Repetitive nature: In every business, some transactions are similar and repetitive in nature. It will be more convenient to record all similar transactions at one place. For example, all credit sales transactions are recorded in the sales book.

- Economical: It is more economical as recording through the special purpose books saves time and also enhances the efficiency of accountants and clerks.

- Easy posting: If similar transactions are recorded at one place, posting becomes easier.

- Complete information at one place: All information related to purchases, sales, cash receipts, payments, etc. are easily and hassle-free available.

![]()

Question 2.

What is cash book? Explain the types of cash book.

Answer:

Cash Book is a book of original entry. It records all transactions related to receipts and payments of cash and deposits in and withdrawals from a bank in a chronological order. In the debit side of the cash book, the cash receipts are recorded in the cash column while all deposits into bank account are recorded in the bank column. On the contrary, in the credit side of the cash book, all cash payments are recorded in the cash column, while all payments through cheques are recorded in the bank column. Usually, it is prepared on monthly basis. Cash book also serves the purpose of principle book (i.e. cash account and bank account).

a. Single column Cash Book: A single column Cash Book contains one column of amount on both sides, i.e., one in the debit side and other in the credit side. In the single column Cash Book, only cash transactions are recorded. In the debit side of the Cash Book, all cash receipts are recorded, while in the credit side all cash payments are recorded.

b. Double column Cash Book: A double column Cash Book contains two columns of amount, namely cash column and bank column on both sides. In the cash column of Cash Book, all cash receipts and payments are recorded, according to the rule of Real Accounts. All deposits either in cash or through cheques into the bank account of the business are debited in the bank column and al withdrawals of cash and payments through cheques are credited in the bank column.

c. Triple column Cash Book: In a triple column Cash Book, there are three coumns of amount namely, cash, bank and discount. Discount allowed and discount received are recorded in the discount column. While in the debit side, discount allowed is recorded along with the receipts, either in cash or through cheque; whereas, in the credit side, discount received is recorded, along with the payments made either in cash or by issuing cheques.

d. Petty Cash Book: This book is used for recording payment of petty expensed, which are of smaller denominations like, postage, stationery, conveyance, refreshment, etc. is known as petty cash book.

Question 3.

What is contra entry? How can you deal this entry while preparing double column cash book?

Answer:

The transaction that is entered in either sides of the double column or three column cash book, affecting both cash and the bank balances concomitantly is called contra entry. These entries result in increase in cash balances and decrease in bank balances or vice versa. In other words, a debit of bank account leads to a credit of cash account and a credit of bank account leads to a debit of cash account. For example, Rs 200 cash deposited into bank. This transaction increases the bank amount on one hand; whereas, on the other hand reduces together.

The contra entries are denoted by ‘C’

Some transactions that lead to contra entry are given below.

- Opening a bank account

- Depositing cash into bank

- Withdrawal from bank.

Question 4.

What is petty cash book? Write the advantages of petty cash book?

Answer:

Petty cash book is used for recording payments of small expenses, which are of smaller denominations such as postage, stationery, conveyance, refreshment, etc. person who maintains petty cash book is known as petty cashier and these small expenses are termed as petty expenses.

It is prepared by the below given two methods:

- Ordinary system: Under this system, a certain sum of money is given to the petty cashier for the payment of petty expenses. After spending the whole amount, the accounts are submitted by the petty cashier to the main cashier.

- Imprest system: Under this system, a fixed sum of money is given to the petty cashier in the beginning of a period to meet the petty expenses to be incurred in that period.

At the end of the period, the amount spent by petty cashier is reimbursed. So, the petty cahier has the same fixed amount of money in the beginning of the next period.

Advantages of petty cash book

- Simple method: Recording of transactions in a petty cash book is easy. In an analytical petty cash book, there exists separate heads for different petty’ expenses, which makes recording much easier. Recording in a petty cash book does not require formal knowledge of accounting principles and techniques.

- Time saving: Recording in petty cash book saves time and efforts of the chief cashier.

- Efficient control: At the end of a period, petty cash book is audited by the main cashier, so frauds and errors are less probable,

- Convenient handling: Recording in petty cash book is convenient, as entries are to be recorded under separate heads, which makes posting easier and quicker.

Question 5.

Describe the advantages of sub-dividing the Journal.

Answer:

The advantages of sub division of Journal are given below:

a. Division of work: The lack of sub-division of Journal may lead to chaos and confusions, ,

if large numbers of transactions are to be recorded through Journal entry by more than one accountant. The will be more inflexible and lack of accountability among the accountants. Sub-division of Journal into subsidiary books facilitates division of work. Sub-division enables different accountants to work on different books. This will not only avoid confusions but also enhance the sense of accountability among the accountants.

b. Time saving: The art of recording through subsidiary book is time efficient and more

effective as compared to recording through Journal entries.

c. Prompt information: The transactions of similar nature are recorded in a particular

subsidiary book. This acts as read)’ source to access information quicker than through journal entry.

d. Creates atcountability: Sub-division of journal entrusts accountants with higher degree of responsibility and accountability for maintaining subsidiary’ book that are assigned to them.

e. Easy checking: In case discrepancies or errors arise, they can be easily located and rectified, as lesser number of transactions is recorded in a subsidiary book than in a – journal.

f. Specialization: The accountability, responsibility and division of work together enhance the specialization of each accountant. This is because, routine and repetitive tasks are performed by each accountant.

![]()

Question 6.

What do you understand by balancing of account?

Answer:

Accounts are prepared on weekly, fortnightly, monthly, quarterly or on daily basis. At the end ; of each period they are balanced. The balancing of the accounts is done in the manner given below: –

- The totals of the debit and credit of an account is calculated, to ascertain which one them is higher.

- The higher figure among debit and credit side is written in the grand total cello on both sides of the account, i.e., in debit and in credit side.

- The next step is to ascertain the difference between the debit total and the credit total. This difference is called ‘Closing Balance’ or ‘Balance carried down’, and is denoted by‘Balance c/d’.

- The ‘Balance c/d’ will be shown either in the debit or credit side, whichever totals up into lower amount.

- If ‘Balance c/d’ is written in the debit side, then the balance is called ‘Credit balance’. On the other hand, if ‘Balance c/d’ is written in the credit side, then the balance is called ‘Debit Balance’.

- On closing the account, ‘Balance c/d’ is brought forward to the subsequent period, and it is written as ‘Balance b/d’.

Usually, the closing balances of real and personal accounts are forwarded to the next period by this manner. For nominal accounts, Step lto 3 remain same and they are closed by transferring the closing balances either to Trading Account or to Profit and Loss Account.

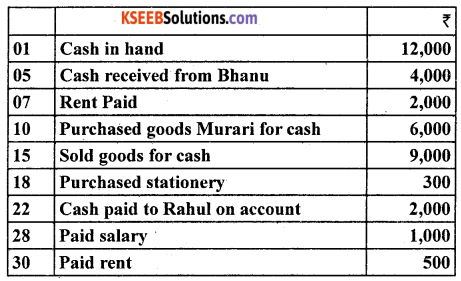

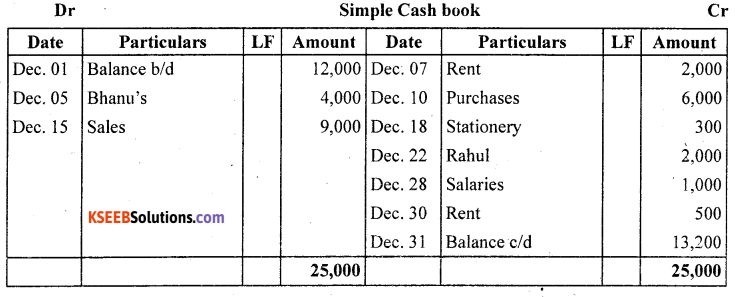

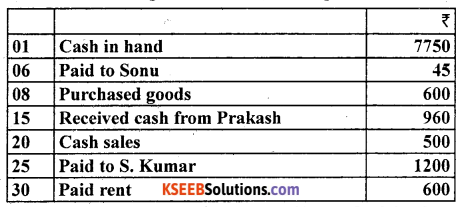

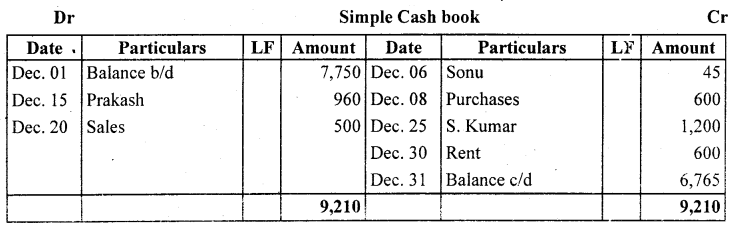

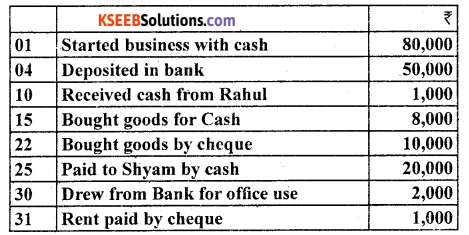

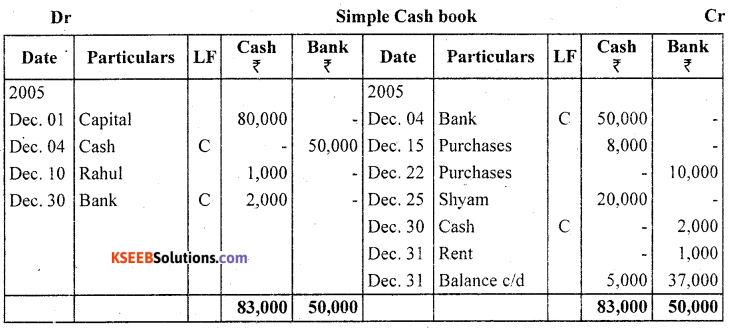

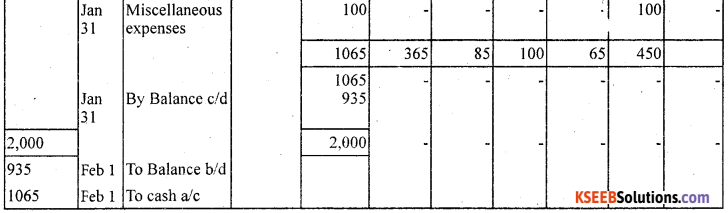

Question 7.

Enter the following transactions in a simple cash book for December 2014

Answer:

Answer:

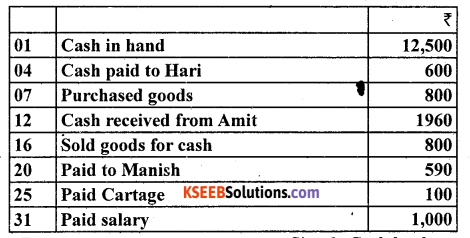

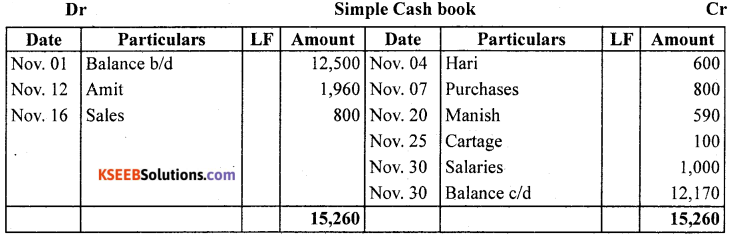

Question 8.

Record the following transactions in a simple cash book for November 2014

Answer:

Question 9.

Enter the following transactions in a simple cash book for December 2014

Answer:

Question 10.

Record the following transactions in a bank column cash book for December 2014

Answer:

![]()

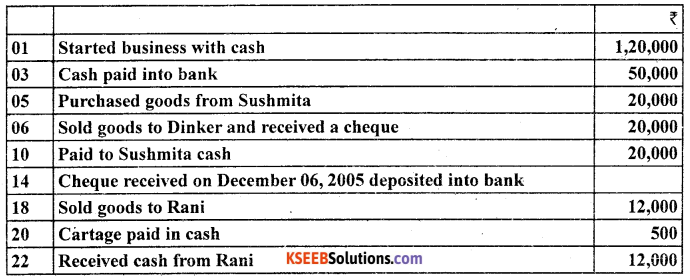

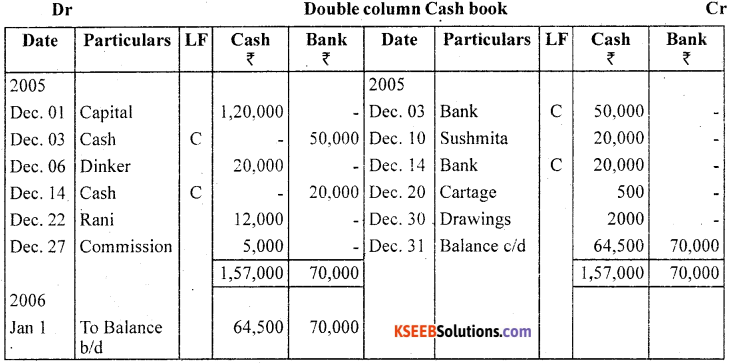

Question 11.

Prepare a double column cash book with the help of following information for December 2014

Answer:

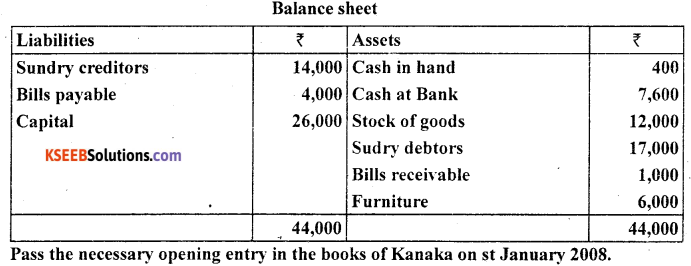

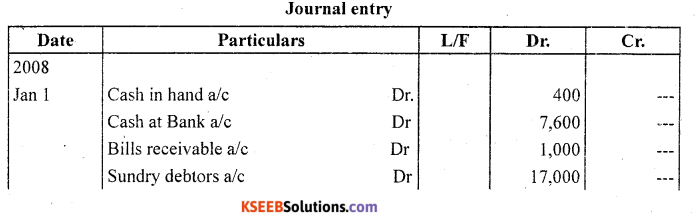

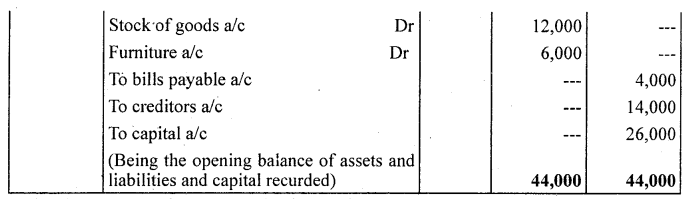

Question 12.

The following is the balance sheet of Mr. Kanaka as on 31st December 2007.

Answer:

Question 13.

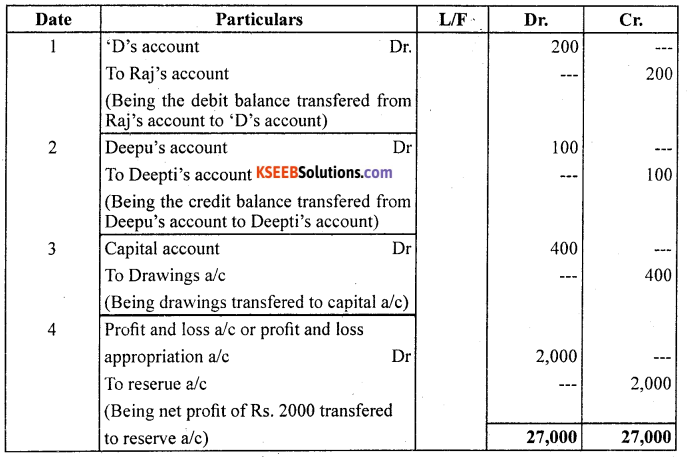

Write the necessary journal entries for the following.

- A debit balance of ₹ 200 from Roy’s account is to be transfered to ‘D’s accounts.

- A credit balance of ₹ 100 from Deepu’s account to be transfered to Deepti’s accounts.

- Drawings of ₹ 400 is transfered to capital account.

- Net profit of ₹ 2,000 is transfered Reserve to a/c.

Answer:

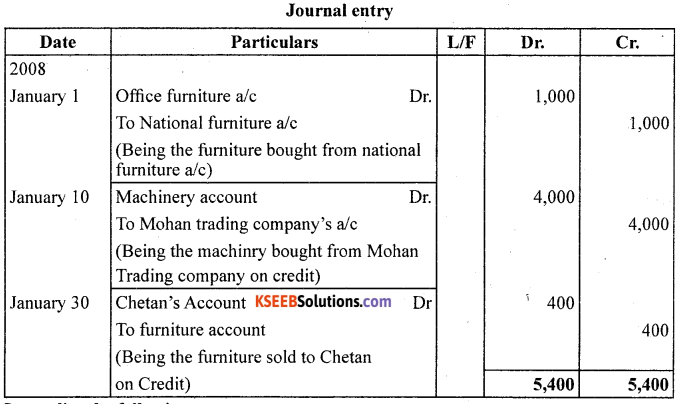

Question 14.

Journalise the following transactions.

2008

Janauary 1 – Bought office furniture form national furniture ₹ 1,000

Janauary 10 – Bought machinery from Mohan trading company ₹ 4,000

Janauary 15 Bought stationery from school Book compnay for ₹ 100

Janauary 30 Sold furniture to Chetan for ₹ 400.

Answer:

![]()

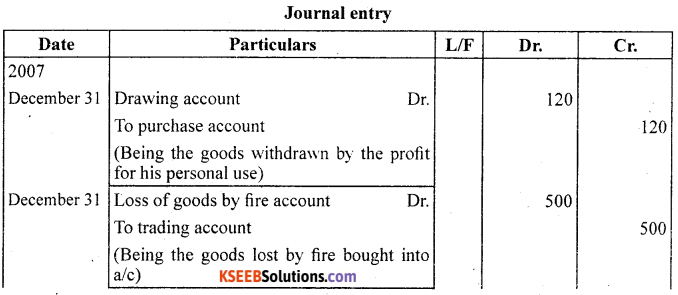

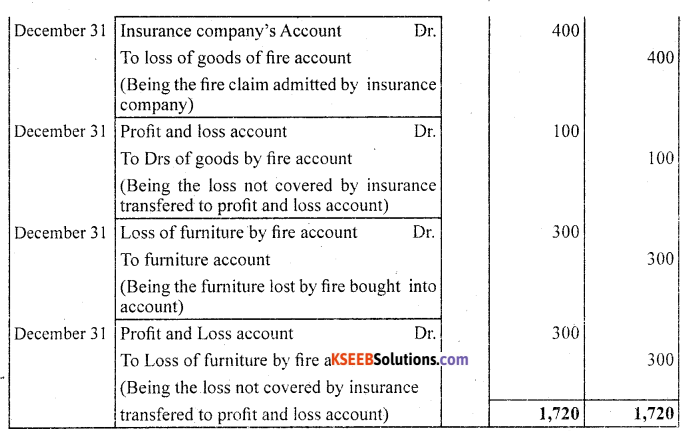

Question 15.

Journalise the following transactons.

2006

December 31 Goods withdrawn by the proprietors for his personal use ₹ 120.

December 31 Goods of the value of ₹ 500 were destroyed by the insurance company was ₹ 400.

December 31 Furniture of the value of ₹ 300 was last by fire.

Answer:

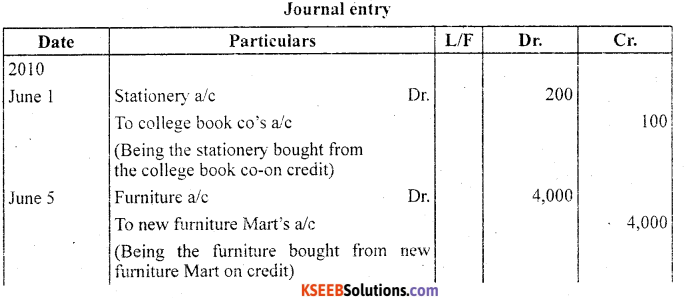

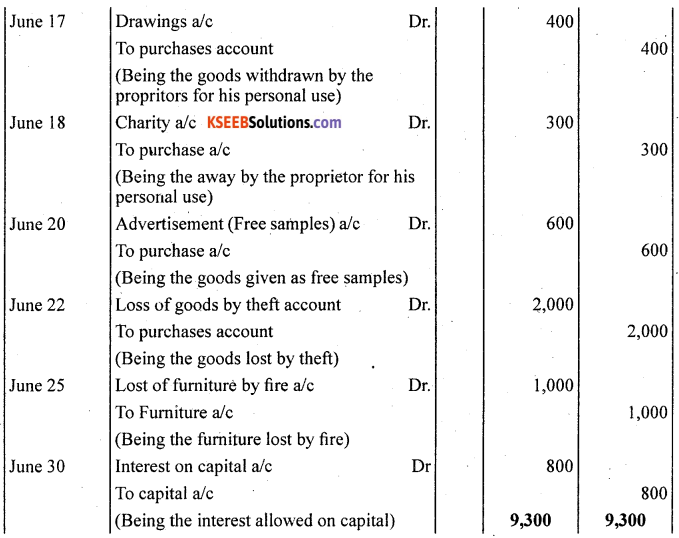

Question 16.

Enter the following transactions in the journal proper.

2000

June 1 – Purchased stationery from college book company on credit ₹ 200.

June 5 – Bought furniture from new furniture ‘Mart’ ₹ 4,000.

June 17 – goods withdrawn by the propritor for his personal use ₹ 400.

June 18 – Goods given away as charity ₹ 300.

June 20 – Goods given as free samples ₹ 600.

June 22 – Goods lost by theft ₹ 2,000.

June 25 – Furniture los by fire ₹ 1,000.

June 30 – Interest on capital ₹ 800.

Answer:

Question 17.

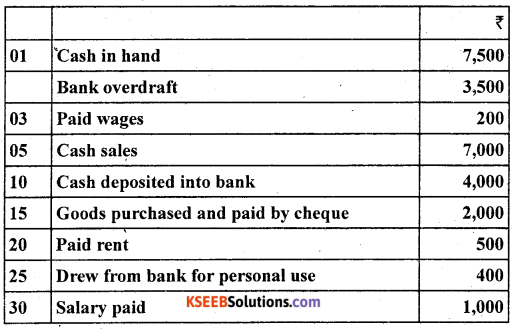

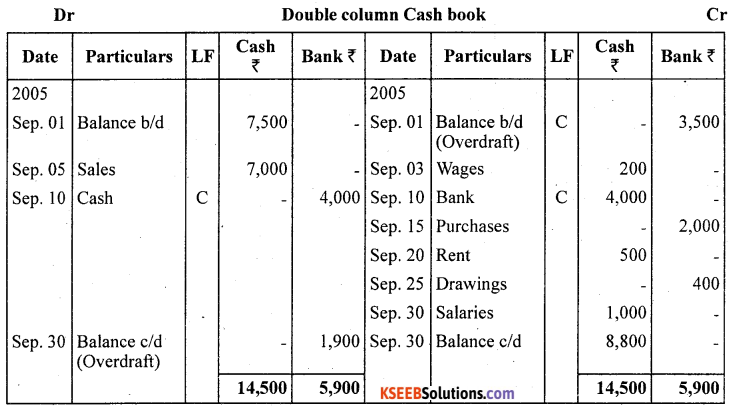

Prepare double column cash book from the book from the following information for september 2014

Answer:

Question 18.

Enter the following transaction in a double column cash book of M/s Mohit Traders for January 2014

Answer:

1st PUC Accountancy Recording of Transactions II Twelve Marks Questions and Answers

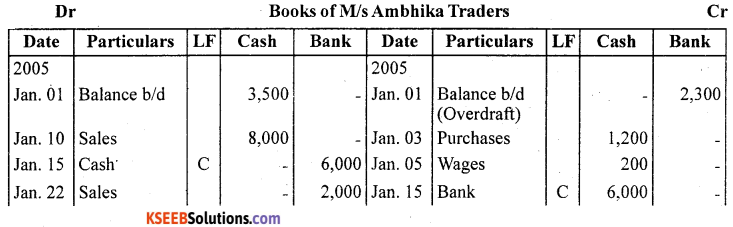

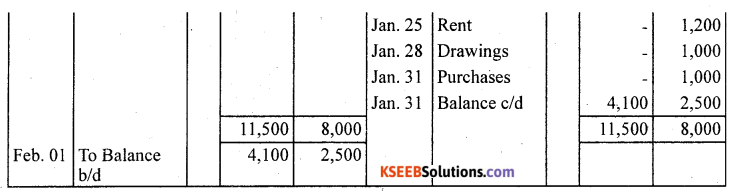

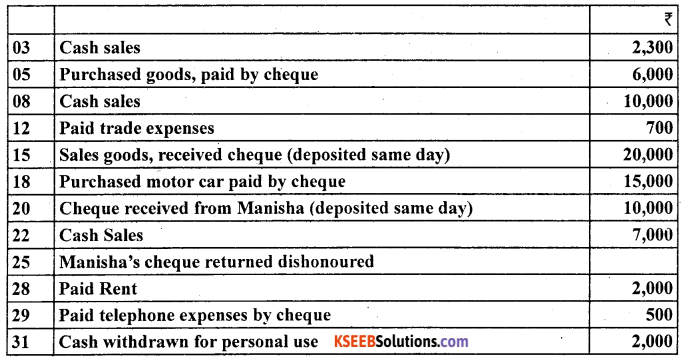

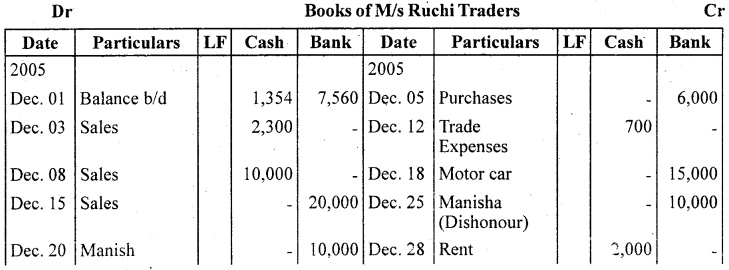

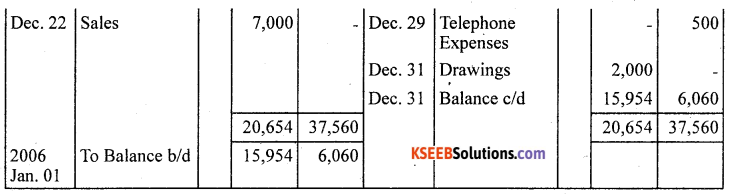

Question 1.

M/s Ruchi trader started their cash book with the following balances on Dec. 01 2010: cash in hand ₹ 1,354 and balance in bank current account ₹ 7,560. He had the following transaction in the month of December 2014

Answer:

![]()

Question 2.

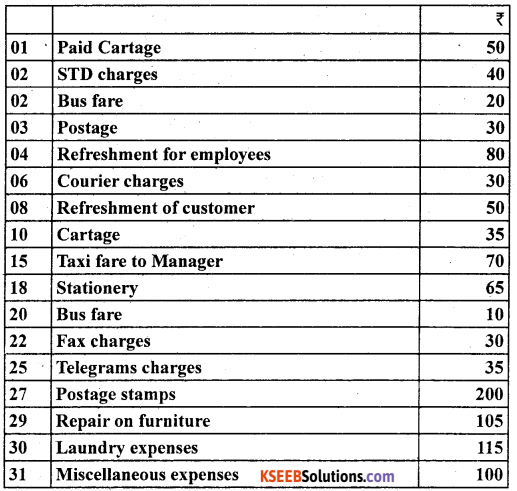

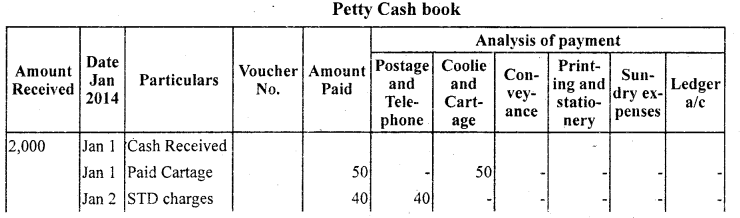

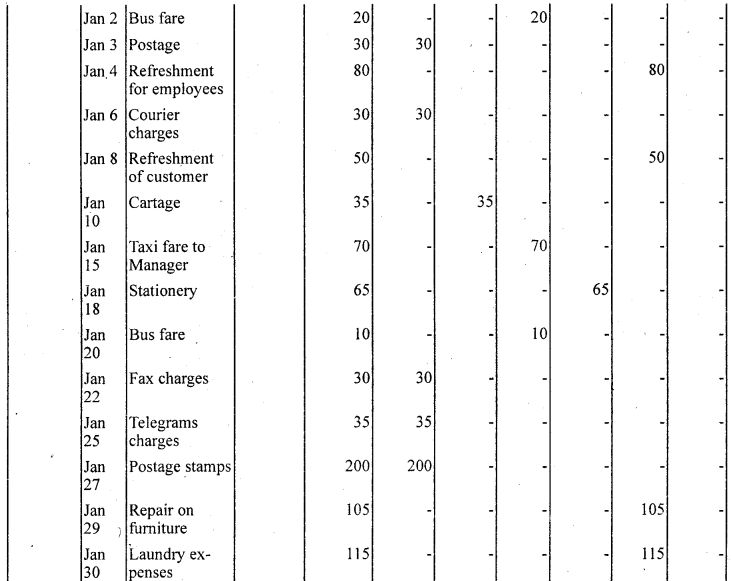

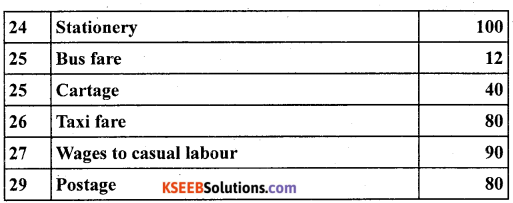

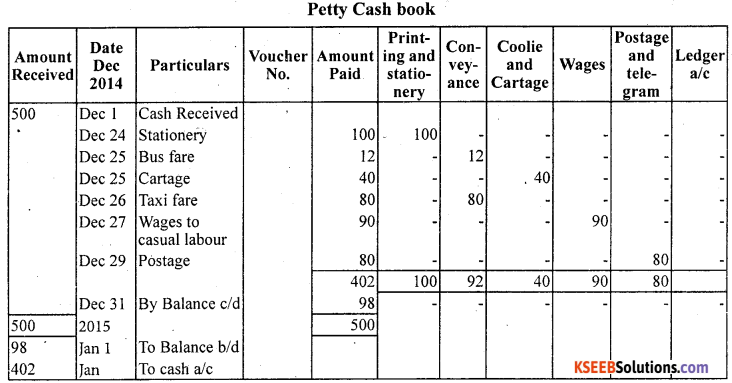

Prepare petty cash book from the following transactions. The imprest amount is ₹ 2,000.

Answer:

Question 3.

Record the following transactions during the week ending Dec. 30,2014 with a weekly, imprest ₹ 500.

Answer:

Question 4.

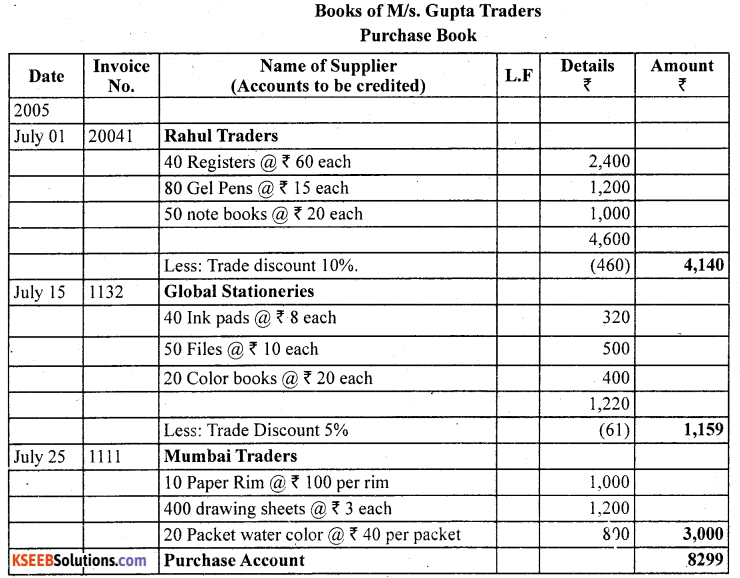

Enter the following transactions in the Purchase Journal (Book) of M/s Gupta Traders of July 2005:

01 Bought from Rahul Traders as per invoice no. 20041

40 Registers @ ₹ 60 each

80 Gel Pens @ ₹ 15 each

50 note books @ ₹ 20 each

Trade discount 10%.

15 Bought from Global Stationers as per invoice no. 1132

40 Ink pads @ ₹ 8 each

50 Files @ ₹ 10 each

20 Color books @ ₹ 20 each

Trade Discount 5%

25 Bought from Mumbai Traders as per invoice no. 1111

10 Paper Rim @ ₹ 100 per rim

400 drawing sheets @ ₹ 3 ach

20 Packet water color @ ₹ 40 per packet

Answer:

Question 5.

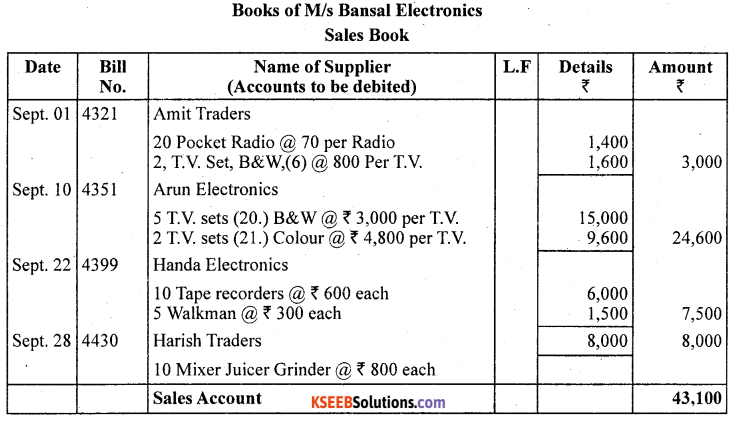

Enter the following transactions in Sales(Journal) Book of M/s Bansal electronics September:

01 Sold to Amit Traders as per bill no. 4321

20 Pocket Radio @ 70 per Radio

2, T.V. Set, B&W,(6) @ 800 Per T.V.

10 Sold to Arun Electronics as per bill no. 4351

5 T.V. sets (20.) B&W @ ₹ 3,000 per T.V.

2 T.V. sets (21.) Colour @ ₹ 4,800 per T.V.

22 Sold to Handa Electronics as per bill no. 4,399

10 Tape recorders @ ₹ 600 each

5 Walkman @ ₹ 300 each

25 Sold to Harish Trader as per bill no. 4430

10 Mixer Juicer Grinder @ ₹ 800 each.

Answer:

![]()

Question 6.

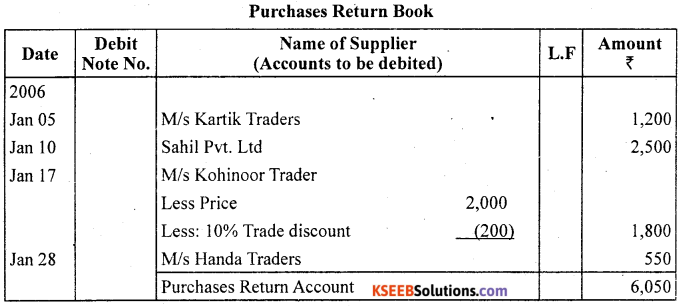

Prepare a purchases return (journal) book from the following transactions for January 2006.

05 – Returned goods to M/s Kartik Traders

10 – Goods returned to Sahil Pvt. Ltd.

17 – Goods returned to M/s Kohinoor Traders for list price ₹ 2,000 less 10% trade discount.

28 – Return outwards to M/s Handa Traders

Answer:

Question 7.

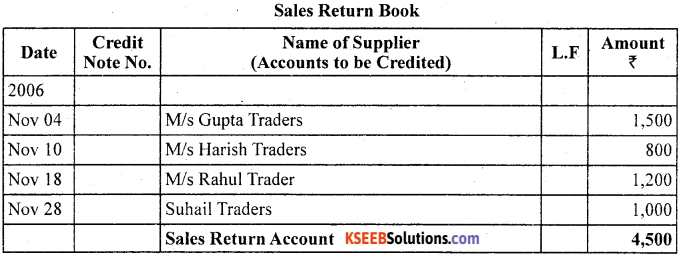

Prepare Return Inward Journal (Book) from the following transactions of M/s Bansal Electronics for November 2005:

04 – M/s Gupta Traders returned the goods

10 – Goods returned from M/s Harish Traders

18 – M/s Rahul Traders returned the goods not as per specifications

28 – Goods returned from Sushil Traders

Answer:

Question 8.

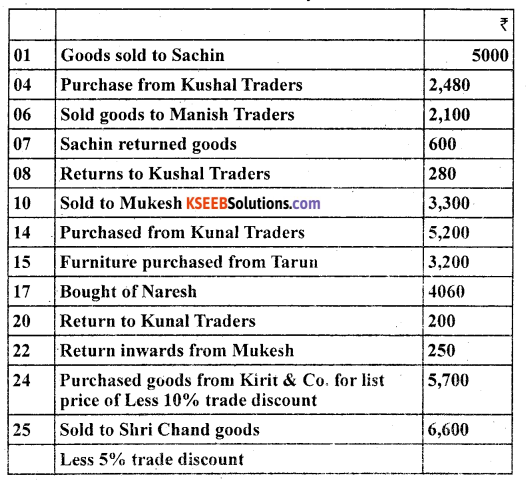

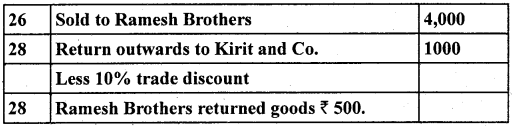

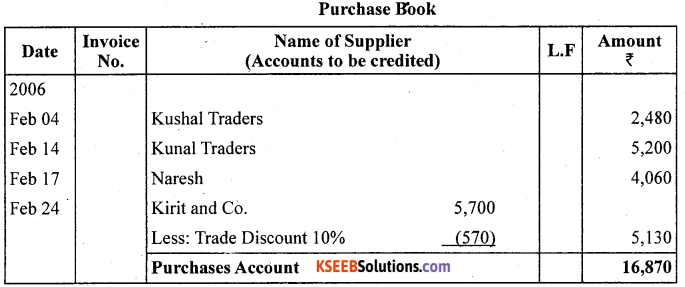

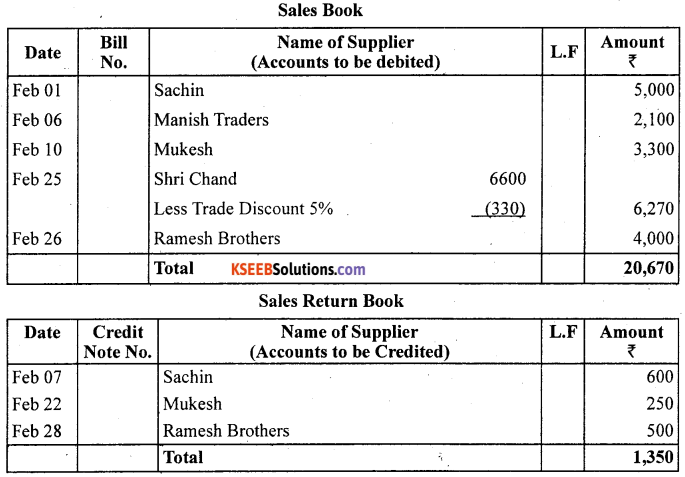

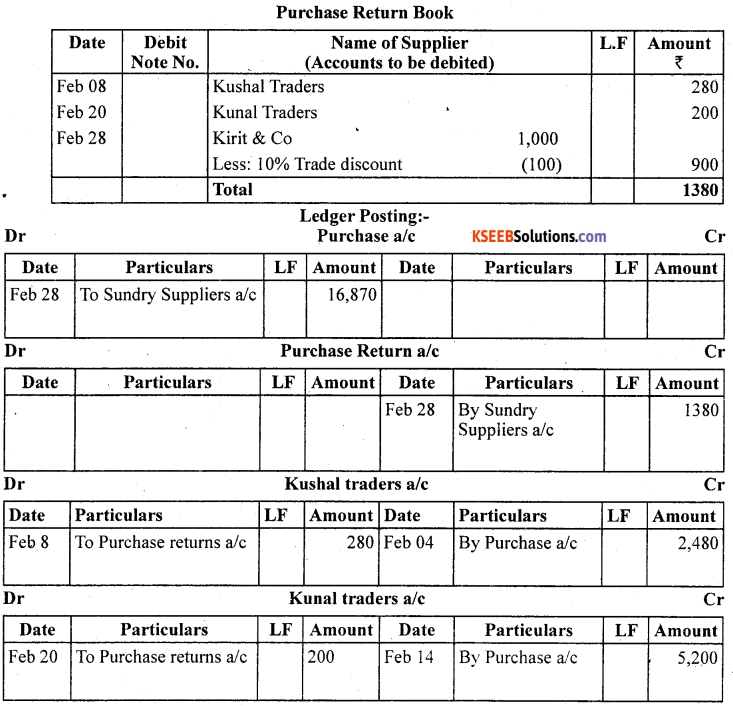

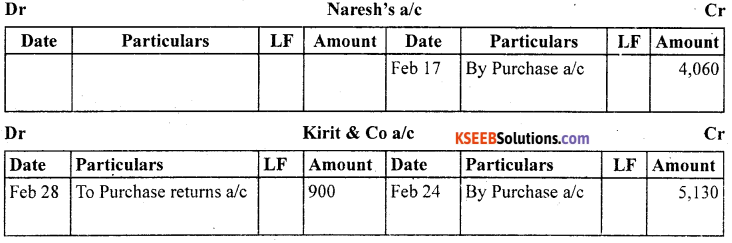

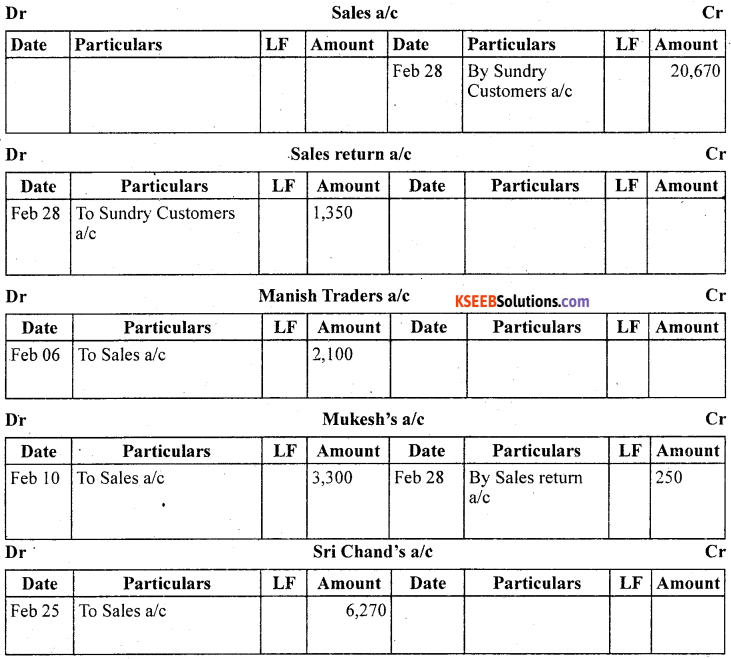

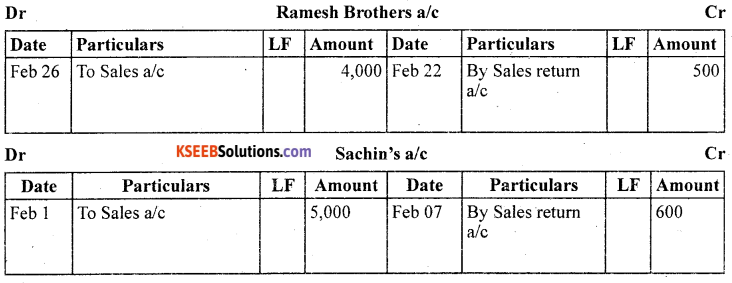

Prepare proper subsidiary books and post them to the ledger from the following transactions for the month of February 2014:

Answer:

![]()

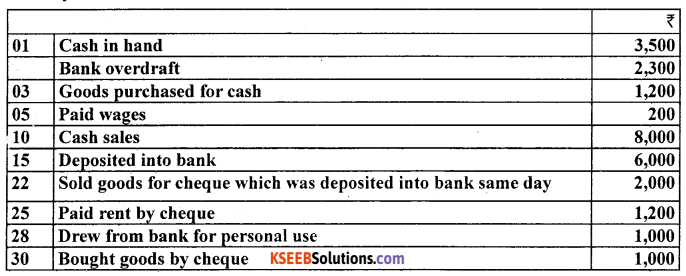

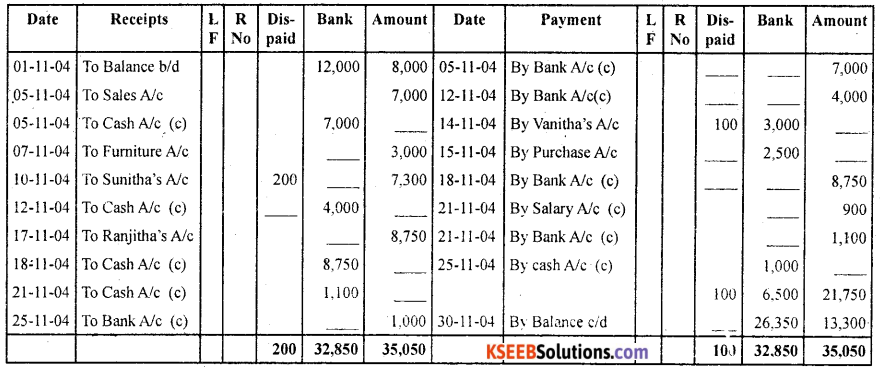

Question 9.

Draft a triple coloumn cash book:

01.11.2004 – Balance of cash in hand ₹ 8,000 and at Bank ₹ 12,000

05.11.2004 – Cash sales and banked the money ₹ 7,000

07.11.2004 – Sold old furniture for cash ₹ 3,000

10.11.2004 – Received from Sunitha ₹ 7,300 and allowed her discount ₹ 200

12.11.2004 – Paid into bank ₹ 4,000

14.11.2004 – Paid to Vanitha by a cheque X 3,000 and received discount of ₹ 100

15.11.2004 – Purchase goods for ₹ 2,500 by cheque

17.11.2004Received a cheque from Ranjitha for ₹ 8,750

18.11.2004 – Deposited Ranjitha’s cheque into bank for collection

21.11.2004 – Paid salary by cash X 900 and sent by cheque ₹ 1,100

25.11.2004 – Drawn from bank for office use ₹ 1,000

Answer:

Three Coloumn cash book for the month of November 2004.

Question 10.

Write up a three column cash book of Mr. Joseph from the balance the swame at the end of the month.

Answer:

Question 11.

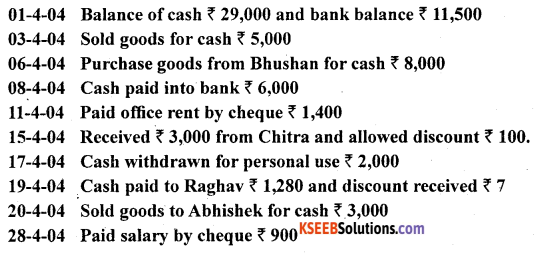

Enter the following transactions in a three column cash book:

01-4-04 – Balance of cash ₹ 29,000 and bank balance ₹ 11,500

03-4-04 – Sold goods for cash ₹ 5,000

06-4-04 – Purchase goods from Bhushan for cash ₹ 8,000

08-4-04 – Cash paid into bank ₹ 6,000

11-4-04 – Paid office rent by cheque ₹ 1,400

15-4-04 – Received ₹ 3,000 from Chitra and allowed discount ₹ 100.

17-4-04 – Cash withdrawn for personal use ₹ 2,000

19- 4-04 – Cash paid to Raghav ₹ 1,280 and discount received ₹ 7

20- 4-04 – Sold goods to Abhishek for cash ₹ 3,000

28-4-04 – Paid salary by cheque ₹ 900

31-4-04 – Paid advertisement ₹ 1,050

Answer:

Question 12.

Enter the following transactions in the proper Subsidiary Books:

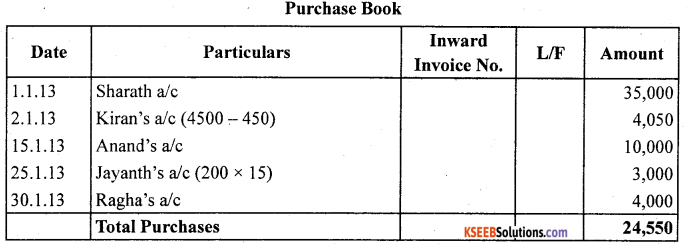

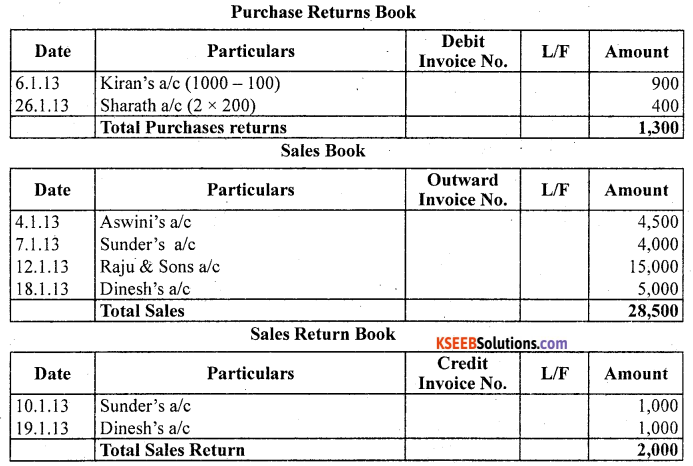

2013 January

Jan 01 – Purchased goods from Sharath ₹ 3,500.

Jan 02 – Bought from Kiran ₹ 4,500 on account, less 10% discount. Jan 04 Sold goods to Ashwin ₹ 4,500.

Jan 06 – Returned defective to Kiran ₹ 1,000 (Gross).

Jan 07 – Sold goods to Sunder ₹ 4,000.

Jan 10 – Returned defective goods by Sunder ₹ 1,000.

Jan 12 – Credit sales to Raju and Sons ₹ 15,000.

Jan 15 – Credit purchases from Anand ₹ 10,000.

Jan 18 – Dinesh bought from us on account ₹ 5,000.

Jan 19 – Sent a credit note to Dinesh ₹ 1,000.

Jan 24 – Cash sales to Vinay ₹ 3,000.

Jan 25 – Bought 15 units from Jayanth @ ₹ 200 per unit.

Jan 26 – Returned to Jayanth 2 damaged units.

Jan 30 – Purchases from Raghu ₹ 4,000.

Answer:

![]()

Question 13.

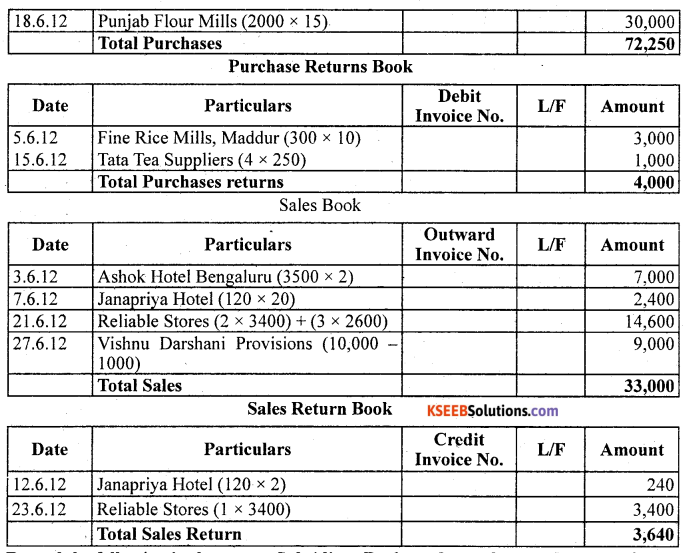

Record the following in the proper Subsidiary Books of Dinanithyada Provisions Stores for the month of June 2012.

2012 June

Jun 01 – Purchased 10 bags of rice from Fine Rice Mills, Maddur at ₹ 3,600 per bag.

Jun 03 – Sold 2 bags of sugar to Ashok Hotel, Bengaluru at ₹ 3,500 per bag.

Jun 05 – Sent a debit note to Fine Rice Mills, Maddur for the overprice of ₹ 300 per bag.

Jun 07 – Sold 20 kgs. of coffee to Janapriya Hotel at ₹ 120 per kg.

Jun 10 – Purchased 25 cases of tea from Tata Tea Suppliers for ₹ 6,250.

Jun 12 – Sent a credit note to Janapriya Hotel for short supply of 2 kgs. coffee.

Jun 15 – Returned 4 cases of tea to Tata Tea Suppliers for defective.

Jun 18 – Bought 15 bags of wheat flour from Punjab Flour Mills at ₹ 2,000 per bag.

Jun 21 – Supplied 2 bags of rice and 3 bags of wheat flour to Reliable Stores respectively at ₹ 3,400 per bag and ? 2,600 per bag.

Jun 23 – Reliable Stores returned wrong supply of 1 bag of rice.

Jun 26 – Bought office Furniture from Carved Furniture Mart of ₹ 25,000 on credit.

Jun 27 – Sold to Vishnu Darshani Provisions of ₹ 10,000 on account, less 10% discount.

Answer:

Question 14.

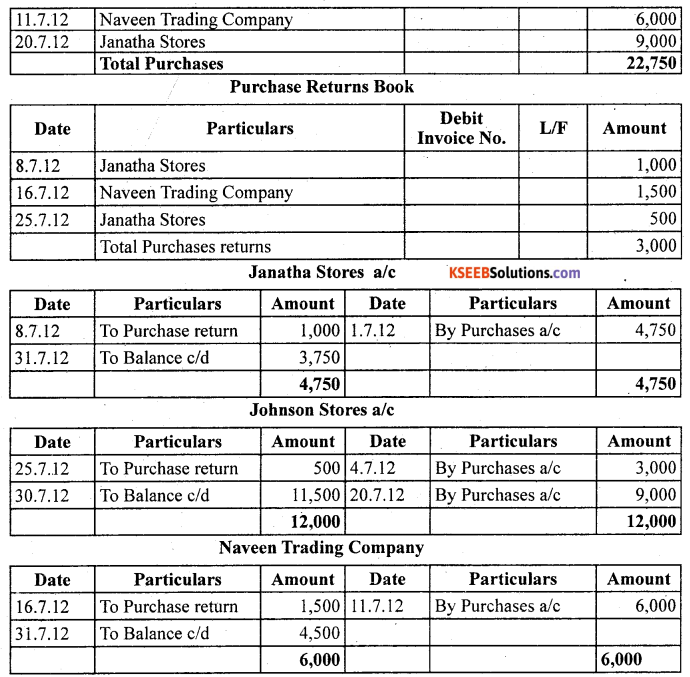

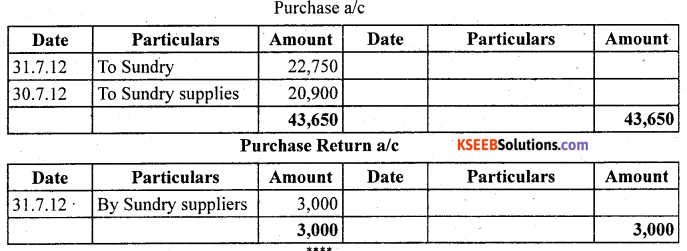

Record the following in the proper Subsidiary Books and post them to the ledger for the month of July 2012.

2012 July

July 01 – Bought from Janatha Stores ₹ 5,000 @ 5% disount.

July 04 – Purchased from Johnson Stores ₹ 3,000 on account.

July 08 – Returned to Janatha Stores damaged goods ₹ 1,000.

July 10 – Sent an order to Naveen Trading Company ₹ 6,000.

July 11 – Received goods from Naveen Trading Company as per the order.

July 16 – Returned to Naveen Trading Company defective of ₹ 1,500.

July 20 – Bought from Johnson Stores goods of ₹ 9,000 on account.

July 25 – Sent a debit note to Johnson Stores for short supply of ₹ 500.

July 28 – Cash purchases from Nandini Shop ₹ 3,150.

Answer:

![]()