Karnataka 2nd PUC Economics Important Questions Chapter 4 The Theory of The Firm and Perfect Competition

Very Short Answer Type Questions

Question 1.

What is market?

Answer:

In Ecnomics ‘Market’ refers to an arrangement where buyers (consumers) and sellers (firms) come in contact with each other directly or indirectly to buy or sell the goods.

Question 2.

Who is a price taker?

Answer:

A “firm” is called as price taker in perfect competition.

Question 3.

What do you mean by revenue?

Answer:

The revenue refers to the money received by a firm from the sale of a given quantity of commodity in the market.

Question 4.

How do you calculate the average revenue?

Answer:

The average revenue can be calculated as

AR = \(\frac{\text { Total Revenue }}{\text { q (Number of Unit Sold) }}\)

Question 5.

Give the meaning of supply?

Answer:

The term supply means the quantity of a commodity offered for sale at a given price at a given period of time.

![]()

Question 6.

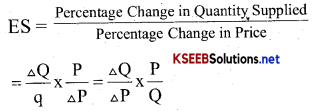

Write the formula to calculate the price elasticity of supply?

Answer:

Price elasticity supply = \(\frac{\text { proportionate change in supply }}{\text { Proportionate change in price }}\)

Question 7.

MR = TR -?

Answer:

MR = TRn – TRn-1

Question 8.

What is meant by price mechanism?

Answer:

The process of determination of price by supply and demand forces is called a price mechanism.

Question 9.

What is equilibrium?

Answer:

Equilibrium means a state of position of rest or state of balance.

Question 10.

What do you mean by equilibrium price?

Answer:

Equilibrium price refers to where quantity of demand and supply will be equal, where both the buyer’s and seller’s objectives are satisfied.

Question 11.

Can MR be negative or zero?

Answer:

Yes, MR can be zero or negative.

Question 12.

What is price line?

Answer:

Price line is the same as AR line and is horizontal to x axis in perfect competition.

Question 13.

Define perfect competition?

Answer:

Perfect competition is a market with large number of buyers and sellers, selling homogeneous product at same price.

Question 14.

What do you mean by abnormal profit?

Answer:

It is the situation for the firm when TR > TC.

![]()

Question 15.

Why AR is equal to MR under perfect competition?

Answer:

AR is equal to MR under perfect competition because price is constant.

Question 16.

What is normal profit?

Answer:

Normal profit is the minimum amount of profit which is required to keep an entreprenuer in production in the long run.

Question 17.

What is the break-even price?

Answer:

In a perfectly competetive market, the break-even price is the price at which a firm earns normal proifit (Price = AC).

In the long run, Break – even price is that price where P = AR = MC.

Question 18.

What are advertisement costs?

Answer:

Advertisement cost are the expenditure incured by a firm for the promotion of its sales such as Publicity through TV, Radio, News paper, Magazine’s and Internet etc…

Question 19.

What is short period?

Answer:

Short period refers to that much time period when quantity of output can be changed only by changing the quantity of variable input and fined factors remaining same.

Question 20.

Define long period?

Answer:

Long-period refers to that much time period available to a firm in which it can increase its output by changing its fixed and variable inputs.

Short Answer Type Questions

Question 1.

Distinguish between firm and industry?

Answer:

Firm:

- Firm is a single unit of an industry.

- Each firm is a price taker in perfect competitioa

- Existence only one firm.

- No separete rules and regualtions are formulated for a firm.

Industry:

- Where the industry is a major unit that consists of many small firms.

- Whare an industry is a price maker in perfect competition.

- There can be many firms in one industry.

- Rules and regulations are made for the industry.

Question 2.

Write the three essentials of a market?

Answer:

The three essentials of a market are as follows:

- Existence of buyers and sellers.

- Commodity which is dealt with.

- Prevalance of a price.

Question 3.

List the determinant elements of market structure?

Answer:

- The number of firms producing a product.

- Nature of the products – homogenous or heterogenous.

- A firm’s freedom to enter and exit from the industry.

Question 4.

A firm in a perfect competitive market is a price – taker? Why?

Answer:

Because no single firm is in a position to influence the price level. Each firm must accept the existing market price hence a firm will be a price taker.

Question 5.

What is meant by shut down point?

Answer:

The point where SMC curve cuts AVC curve at the minimum is called the short run shut down point of the firm.

![]()

Question 6.

Name any four determinants of supply?

Answer:

The four determinants of supply are:

- Technological progress.

- Input prices.

- Tax policy of the government.

- Climatic conditions.

Question 7.

State the law of supply?

Answer:

According to the law of supply other things remaining the same, as the price of commodity increases its supply increases and as the price decreases the supply also decreases.

Question 8.

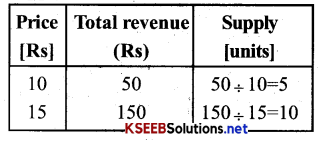

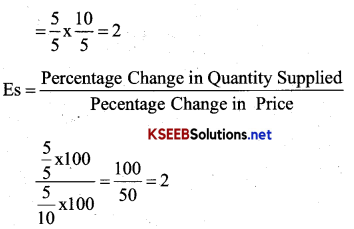

If the price of potato increases from Rs 25 per kg, the quantity offered for sale in the market increases from 100kg to 120 kg. Find the price elasticity of supply.

Answer:

Question 9.

What is invsible hand, according to Adam smith?

Answer:

Adam smith calls price mechanism as ‘Invisible hand’ is always at work, if there is any imbalance it directs and guides both producers and the consumer equilibrium.

Long Answer Type Questions

Question 1.

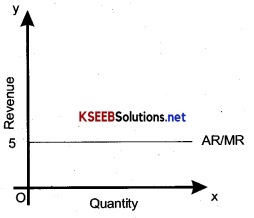

Why is the average revenue of a firm under perfect competition paralled to x – axis & negatively sloped under monopoly?

Answer:

Shape of average revenue curve under perfect competition:

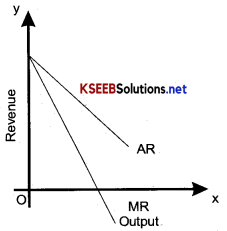

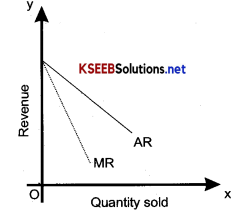

The price of commodity is determined by the force ofdemand & supply. It is determined by the industry. No industrial firm can make its own price. A firm can sell any amount of the commodity at this price as it is price taker instead of price maker. The marginal revenue equals their average revenue and their curves co inside as it is clear from the following schedule and figure.

Shape of AR curve under monopoly in this a firm can cell more by lowering the price of its output. Thus the firm will have a down ward sloping curve. AR and MR curve would be downward sloping but less elastic. It can be explained with the help of the following table and figure:

A monopoly firm has a less elastic down ward sloping AR curve meaning there by that when such a firm raises the price of its product, demand falls less than proportionetly.

Shape of AR are under monopolistic competition demand (AR) curve of a firm in the monopolistic competition is also negetively sloped indicating that a large amount of the commodity can be sold only at a lower price. In the other words average revenue curve under monopolistic competition is similar to that under monopoly as shown below with the help of a table and a diagram.

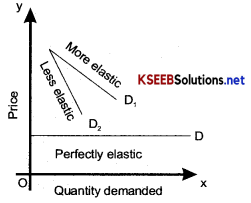

(An average curve in a single diagram- Average revenue curves under diflrent market situations have been shown in a single diagram. In perfect competition AR is perfectly elastic.In monopoly it is less elastic & more in monopolistic competition.

Question 2.

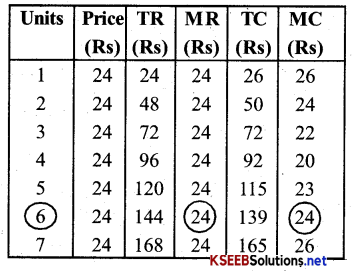

Explain producer’s equilibrium with the help of marginal cost & marginal revenue schedule.

Answer:

Producer’s equilibrium: AProducer is at equilibrium when two following conditions are satisfied.

- Marginal revenue and marginal cost

- Marginal cost must be increasing at profit maximizing output.

Producers equilibrium has been explained with the help of marginal cost and marginal revenue schedule.

In the above table, MR (Price) is equal to marginal cost at two output units viz 2 units & 6 units. But the producer will be at equlibrium at the level of output which marginal cost increases after being equal to MR. Hence producer will be at equilibrium at 6th output level.

Question 3.

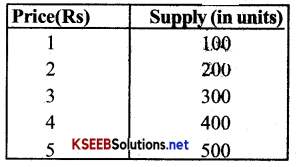

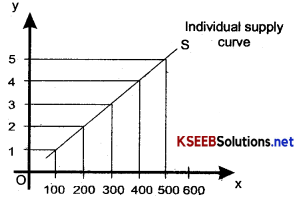

What do you mean by supply? Explain the law of supply schedule & supply curve.

Answer:

Supply : Supply is a quantity of a commodity which a firm is willing to see in the market in a given period of time at a ,given price.

Factors considered constant: Factors like goods of a firm, the price of other commodities, state of technology, prices of factors of production, nature of commodity are considered constatnt while explaining the law of supply.

This can be shown with the help of a schedule

Induvidual schedule supply

The supply schedule & supply curve stated above show that the quantity supplied is increased with rise in price fall with Ms in the price of commodity.

Question 4.

Why does the supply curve slope upwards?

Answer:

Reasons for supply curve sloping upwards: Following are the reasons for supply curve sloping or the operation of law of supply.

1. Rise in profit:

With the increase in the price of a commodity a firm’s profit rises. Consequently a firm produces more quantity of a commodity to increase its amount of profit.

2. Entry of new firms:

A rise in the price increases the profit Increase in profit attracts new firms to enter the industry & adds to the supply of commodity.

3. Keeping low stock:

The increase in price of a commodity induces the sellers to keep a least stock and sell more.

Question 5.

Write down the causes for the increase and decrease in the supply.

Answer:

Causes for increase in supply:

- Fall in the remuneration of factors of production.

- Improvement in technology.

- Change in the good of production.

- Taxation policy of the government.

- Fall in the prices of the other commodities.

- Increase in subsidies.

Causes in decrease in supply

- Rise in the prices of other commodities.

- Rise in the remuneration of factor of production.

- Technology becoming outdated.

- Change in the objectives of producers.

- Taxation policy of goods.

- Decrease in subsidies.

![]()

Question 6.

How many methods are there to estimate the elasticity of supply? Explain any one method.

Answer:

There are two methods of measuring elasticity of supply:

- Proportional method &

- Geometric method

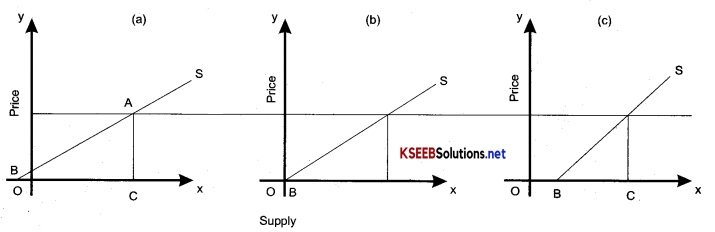

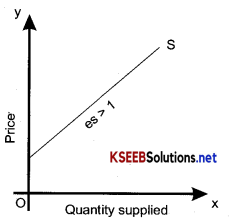

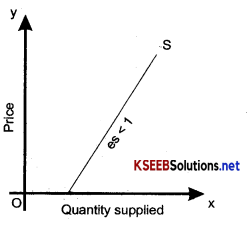

Geometric method of measuring elasticity of supply: Under this method apoint is taken on the straight line supply curve and is extended to meet the x-axis. Then the supply curve is extendd to meet the x-axis. This distance is divided by the quantity supplied. The quotient will be elasticity of supply. It is mainly explained by taking three different curves.

- In figure a, price elasticity of supply at point A = BC/OC (BC) is distance and OC is quantity supplied.

Here BC > OC Hence ES > 1 - In figure b, elasticity of supply at point A = BC/OC.

Here BC=OC Hence Σs = 1 - In fig C, price elasticity of supply at point A= BC/OC

Here BC< OC, Hence ES < 1

In short we can say that elasticity of supply on straight line supply curve is greater than unit that is ES>1. When the supply curve intersects X-Axus is in negetive range, it is equal to one when the supply curves passes through the origin and it is less than one when the supply curve intersects x-axis in the positive range.

Question 7.

Explain the various types (degrees) of price elasticity of supply.

Answer:

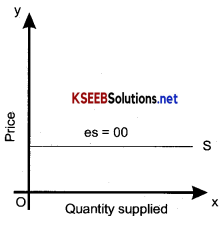

Types or degrees of price elasticity of supply: There are five types (degrees) of price elasticity of supply.

1. Perfectly elastic supply : When there is no change in the price of the commodity, but there is change in the quantity supplied this type of supply curve is obtained in those industries which produces goods under law of constant costs.

| Price (Rs) | Quantity (units) |

| 2 | 200 |

| 2 | 200 |

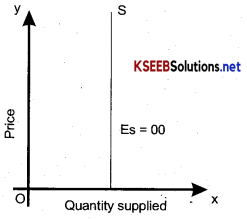

2. Perfectly ¡n elastic supply -When there is a change in the price of the commodity, but there is no change in the quantity supplied.

In this case elasticity of supply is zero (ES = 0)

| Price (Rs) | Quantity (units) |

| 2 | 100 |

| 3 | 100 |

Supply of perisable goods in short period is in elasticity.

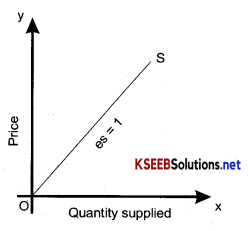

3. Unit elasticity supply: (ES = 1): When the percentage change in the quantity supplied is equal to the pecentage change in price, the elasticity of supply is said to be unitary elasticity of supply. It forms an angle, of 450 It means price and supply change is the same proprtion.

| Price (Rs) | Quantity (units) |

| 2 | 100 |

| 4 | 200 |

4. More than unit elastic supply: In this case, rate of change in quantity offered is greater than rate of change in prce (ES > I)

| Price (Rs) | Quantity (units) |

| 2 | 100 |

| 3 | 200 |

5. Less than unit elastic supply : In this case, rate of change in quantity is smaller then rate of change in price.

| Price (Rs) | Quantity (units) |

| 2 | 100 |

| 4 | 140 |

![]()

Question 8.

Explain the various factors which affect magnitude of price elasticity Following factors affect the magnitude of price elasticity of supply.

Answer:

1. Nature of the commodity: Perisable commodities have an elastic supply, because their supply cannot be increased or decreased , even when price changes. Supply of durable goods is elastic, because their supply cannot be increased or decreased as a result of increase or decrease in price.

2. Cost of production: If production is subject to the law of increasing costs, then supply of such goods will be in elastic. It is difficult to extend supply due to rise in price.

3. Time: Longer the time period, greater will be the elasticity of supply. On the other hand shorter the time period, small will be the elasticity of supply.

4. Availability of facilites for expanding output: Elasticity of supply also depends on the availibihty of facilities for expanding output. Farmers cannot raise their agricultural output with rise in the price of that output of facilities like seeds, fertilizers or irrigation facilities for expansion are not available, in such a case price elasticity of supply will be less.

5. Risk-taking: The elasticity of supply depends on the willingness of enterpreneurs to take risk. If entrepreneurs are willing to take risk supply will be more elastic, on the other hand, if the enterpereneurs hesitate to take risk the supply will be in elastic.

Exercises

Question 1.

What are the characteristics of a perfectly competitive market?

Answer:

Characteristics of a perfectly competitive firm : following are main charecteristics of a perfectly competitive firm:

1. A large number of buyers & sellers: There are a large number of buyers and sellers of the commodity in this market. Each one of them and it cannot exert perceptible influence on prices.

2. Homogenous product; The output of each firm in the market is homogenous, identical or perfectly standardised. As a result, the buyer cannot distinguish between the output of one firm & that of another & is therefore, indiffrent to the particular firm which he buys.

3. Freedom of entry or exit: Entry or exist of the firms into the market is free in the perfect competition market. This means that any new firm is free to start production, if it so whishe & that any existing firm is free to cease production & leave the industry if it so whishes.

4. Perfect mobility: There is perfect mobility of factors of production, geographically as well as occupationally.

5. Perfect knowledge: There is perfect & complete knowldge on the on the part of the market buyers & sellers about the conditions in the market. For a market to be perfect it is essential that all buyers & sellers should be aware ofwhat is happening in any part of the market.

6. Absence of transport cost: In perfect competition, it is assumed that there is no transport cost for common man who may buy from any firms. This ensures existence of a single uniform price of the product.

7. Perfectly classic demand: Demand AR curve is perfectly classic & paralled to x – axis.

8. Price taker: Firm is price taker and industry is the price maker.

Question 2.

How are the total revenue of a firm market price, and the quality sold by the firm related to each other?

Answer:

Relationship between total revenue of a firm market price and the quantity sold by the firm: Total revenue may be defined as total money receipts of the firm from the sale of its total output in a given period of time. It is calculated by multiplying the price per unit of a commodity with the total number of units sold in the market, for example, if a firm sells 200 fans at the rate of Rs 800 per fan, the total revenue will be Rs 160000. In equation.

TR = Price per unit × No of units sold hence, total revenue increases/decreases with the increase/decrease in price in the units sold in the market. The relationship between total revenue, market price & quantity sold have been shown with the following equation

- TR=Price for unit [Market Price] × Unit sold.

- Price per Unit [Market Price] = \(\frac{\mathrm{TR}}{\text { Units Sold }}\)

- Unit Sold = \(\frac{\text { TR }}{\text { Price per unit [Market Price] }}\)

![]()

Question 3.

What is the price line?

Answer:

If in the output price line, we plot the price of the output for different values of output, we get a horizontal straight line. This straight line is known as a price line.

Question 4.

Why is the total revenue curve of a price-taking firm an Upward-Sloping Straight line? Why does the curve pass through the, the origin?

Answer:

Upward shifting straight Line The total revenue curve of price taking firm is upward sloping straight line due to the fact that price of a price taking firm remains constant as shown below:

Question 5.

What is the relation between market price and average revenue for a price taking firm?

Answer:

The price and average revenue for a price-taking firm are equal.

Question 6.

What is the relation between market price and marginal revenue for a price taking firm?

Answer:

For a price taking firm, marginal revenue is equal to price.

Question 7.

What conditions must hold, if a profit maximising firm produces positive output in a competitive market?

Answer:

Following three conditions must hold if a profit maximising firm produces positive output in a competitive market’

- P = MC

- MC is rising

- P ≥ AVC

![]()

Question 8.

Can there be a positive level of output that a profit maximising firm produces in a competitive market at which price is not equal to marginal cost? Give an explanation.

Answer:

Yes, there can be a positive level of output that a profit maximising firm produces & in a competitive market at which price is not equal to marginal cost.

Question 9.

Will a profit maximising firm in competitive market ever produce a positive level of output in the range where the marginal cost is falling?

Answer:

A profit maximising firm in a competitive market will produce a positive level at output in the same where marginal cost in falling. Falling MC means that the cost of producing an additional unit of output tends to reduce. Here price is constant as the firm in working in a competitive market in this case. The diferences between firm’s total revenue and TVC [TVC = Σ MC] tends to increase. It means firms profit increase with the level of output. Then why should a competitive firm not increases output when gross profit is rising.

Question 10.

Will a profit – maximising firm in a competitive market produce a positive level of oiitput in the short run if the market price is less than the minimum of AVC?

Answer:

During a short period, a firm may continue its production even if has to incur losses due to fixed cost. But if market price further falls and losses exceed FC. i.e. The firm is not able to cover even variable cost, production is stopped. It means that the profit – maximization firm in a competitive market will not produce a positive level of output in the short run of the market price is maximum of AVC.

Question 11.

Will a profit – maximising firm in a competitive market produce a positive level of output in the long run if the market price is less than the minimum of AC? Give an explantaion.

Answer:

A profit maximising firm in a competitive market will not produce a positive level of output in the long -run, if the market price is less than the maximum AC. If a firm produces at this level total cost will be more than its revenue resulting in a loss.

Question 12.

What is the supply curve of a firm in the short run?

The short run supply curve of a firm is the upward rising part of SMC from & above the minimumAVC.

Question 13.

What is the supply curve of the firm on the long run?

Answer:

The supply curve of a firm in the long run is the upward rising part of LRMC, from and above the minimum LRAC.

![]()

Question 14.

How does technological progress affect the supply curve of a firm?

Answer:

With the technological progress, the firm can produce more output with the same levels of Inputs, in other words, to produc a given level of output, the firm now requires loss of inputs. As a result, the marginal costs fall, this results in a right ward shift of MC Curve and Supply curve is essantially a segment of MC. Hence with technological progress, the supply curve ofthe firm shifts to the right.

Question 15.

How does the imposition of a unit tax affect the supply curve of a firm?

Answer:

With the imposition of Unit tax, the cost of production increases. This results in the increases in the marginal cost of every unit of output. As a result the MC curve & hence the supply curve shifts to the left. This imposition of a unit tax shifts the supply curve to the left.

Question 16.

How does an increase in input price effect the supply curve of a firm?

Answer:

If the price of an input increases the cost of production increases. As a result the MC curve & hence the supply curve shift to the left. The firm will now employ less of that input and produce less output. Thus with the increase in the input price the supply curve of a firm shifts to the left.

Question 17.

How does an increase in the number of firms in a market affect the market supply curve?

Answer:

With an increase in the number of firms, the Market supply curve shifts to the right.

Question 18.

What does the price elasticity of supply mean? How do we measure it?

Answer:

Price elasticity of supply means the degree of reponsiveness of a quantity supplied of a commodity to change in its price.

Measurement of price – elasticity of supply.

We measure elasticity of supply by dividing the percentage change in quantity supplied by percentage change in price. In equation:

Question 19.

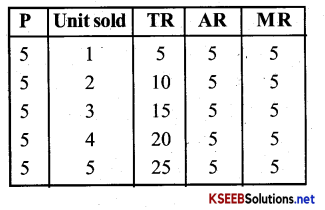

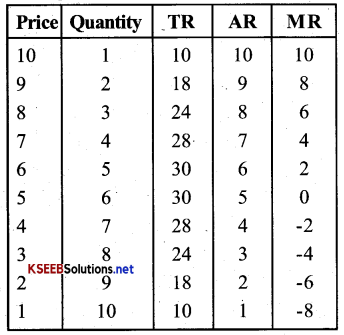

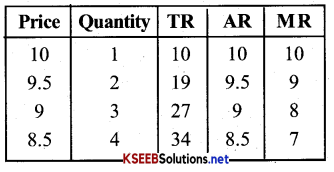

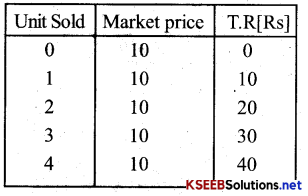

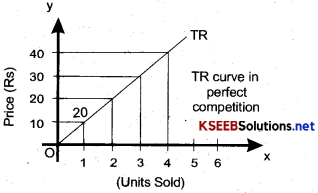

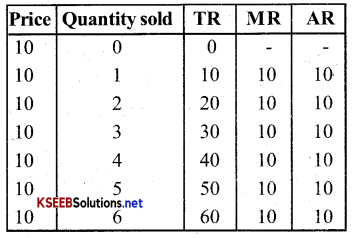

Compute the total revenue, marginal revenue and average revenue schedules in the following table. Market value of price of each unit of the good is Rs 10.

Answer:

Question 20.

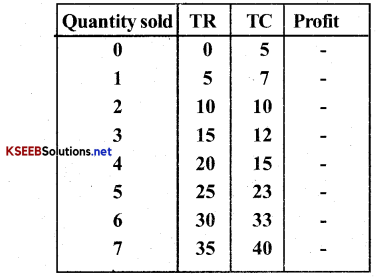

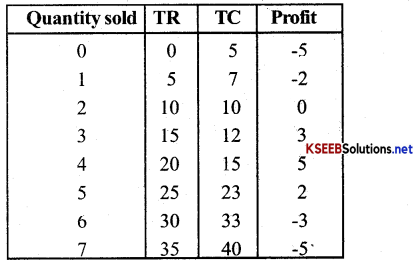

The following table shows the total revenue & total cost of schedule of a compititve firms. Calculate the profit at each level. Determine also the market price of the good.

Answer:

Answer:

![]()

Question 21.

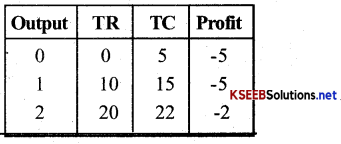

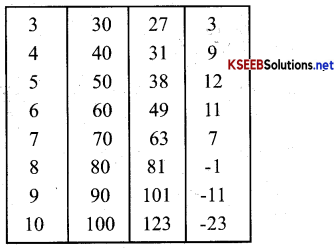

The following table shows the total cost schedule of a competitive firm and given that the price of the good is Rs.10 Calculate the total profit at each level of output. Find the profit maximising level of output.

Answer:

Question 22.

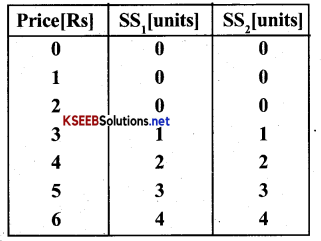

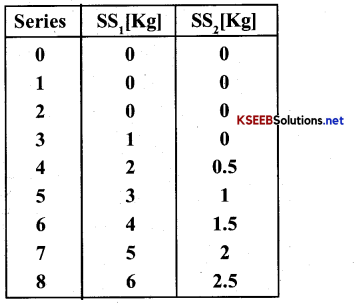

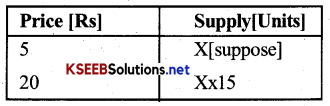

Consider a market with two firms. The following table shows the supply schedules of the two firms. SS1 column gives the supply schedule of firm 1 and the SS2 column gives the supply schedule of firm-2.

Compute the market supply schedule

Answer:

Question 23.

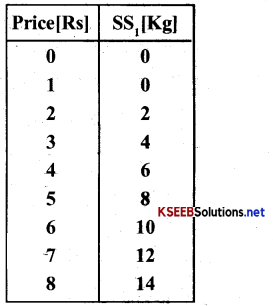

Consider a market with two firms, in the following table columns labelled as SS1 and SS2 give the supply schedules of firm 1 and firm 2 respectively.

Answer:

Question 24.

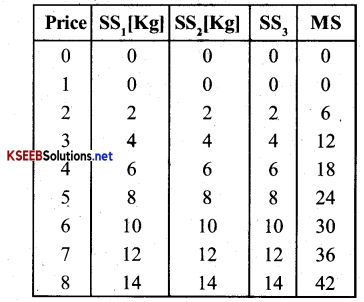

There are three identical firms in a market. The following table shows the supply schedule of firm 1. Compute the market supply schedule.

Answer:

Question 25.

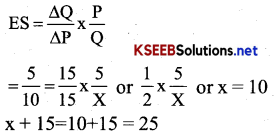

A firm earns a revenue of Rs.50 when the market price of the good is Rs.10. The price increases to Rs.15 and the firm now earns a revenue Rs.150.

Es = \(\frac{\Delta Q}{\Delta P} \times \frac{P}{Q}\)

Question 26.

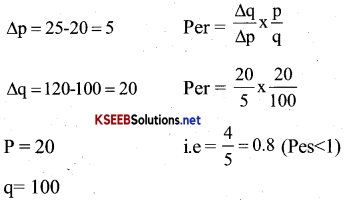

The market price of a good changes from Rs 85 to Rs 8.20. As a result the quantity supplied by a firm increases by 15 units. The price elasticity of the firm’s supply curve is 0.5 Find the initial and fmal output levels of the firm.

Answer: