Karnataka 2nd PUC Economics Important Questions Chapter 3 Production and Costs

Very Short Answer Type Questions

Question 1.

What is average product or average physical product?

Answer:

We may define average product or average physical product as the TPP per unit employment of the variable input.

APP = \(\frac{\mathrm{TPP}}{\mathrm{L}}\)

APP – Average physical pro duct

TPP – Total physical product

L – Where L is the level of employment of the variable input

Question 2.

What is variable input?

Answer:

Variablle input is that input that changes

Question 3.

Give an example for each of fixed factors and variable factors

Answer;

Land and factory building are fixed factors. Where as labour and raw materials are variable factors.

Question 4.

What is meant by production?

Answer:

Transformation of input into output.

![]()

Question 5.

What will be M P when TP is maximum?

Answer:

MP will be zero

Question 6.

Define market period, short-run and long run?

Answer:

Refer time period

Question 7.

When there are diminishing return to a factor total product always decreases?

Answer:

False When there is diminishing return to a factor, TPP increases at a decreasing rate

Question 8.

Increase in TPP always indicates that there are increasing return to a factor?

Answer:

False TPP increases even when there are diminishing return to a factor

Question 9.

When there are diminishing return to a factor marginal and total products always?

Answer:

False. Only MPP falls, not TPP In case of diminishing returns to factor, TPP. increases at diminishing rate

![]()

Question 10.

Why AFC curve never touches the ‘X’axis though it lies very close to X axis?

Answer:

Because TFC can never be zero

Question 11.

Why AVC and AFC always lie below AC?

Answer:

AC is the summation of AVC & AFC, so AC always lies above AVC & AFC.

Question 12.

Why TVC curve starts from the origin?

Answer:

TV,c is zero at zero level of output.

Question 13.

When TVC is zero at zero level of output? What happens to TFC ‘OR’ why TFC is not Zero level of output?

Answer:

Fixed cost are to be incurred even at zero level of output.

Question 14.

What do you mean by cost of production?

Answer:

Cost of production is the expenditure incurred on the input;

![]()

Question 15.

What is meant by fixed or supplementary cost?

Answer:

Fixed cost which do not change when output increases or decreases in the short run, they have to be increased even if the output is 2ero.

Question 16.

Which costs are increased in the fixed cost?

Answer:

Rent for a building / factory/ minimum telephone bill, interest on capital, wages/ salaries to permanent staff are included in the fixed cost.

Question 17.

What is the behaviour of average fixed cost as output increases?

OR

Why does AFC fall as the output rises?

Answer:

AFC is the average fixed cost i,e. FC

AFC = \(\frac{\mathrm{FC}}{\mathrm{Q}}\) with the increase in Q, AFC goes on decreasing.

Question 18.

What is the reson behind ‘U’ shape of MC cruve?

Answer:

The reson behind ‘U’ Shape ofMC curve is operation of law of returns.

Question 19.

When is AC constant and minimum?

Answer:

AC is constant and minimum when MC = AC

![]()

Question 20.

What is revenue?

Answer:

Revenue is the money receipts from the sale of the product.

Short Answer Type Questions

Question 1.

Explain the concept of TP, AP and MP with the help of diagram?

Answer:

Total product:

Total product indicates the total volume of goods & services produced during a specified period of time in a given year

We can calculate total product as follows:

TP = ΣMP

Where ,TP = total product,

Σ MP = sum of marginal product

Average product:

Average product refer to per unit product of a variable factor, It is calculated by dividing the total product by the total number of unit of the variable factor

We can calculate the average product as follows

Total Product

AP = \(\frac{\text { Total Product }}{\text { No, of units of variablefactor }}\) OR \(\frac{\mathrm{TP}}{\mathrm{L}}\)

Marginal product:

Marginal product can be defined as the additional to total product by the employment of an additional unit of a factor.

We can calculate marginal product as follows

MP= TPn – TPn-1

Where MP- Marginal product

TPn – Total product of units

TPn-1 – Total product of n-1 units.

Question 2.

Write down the features of production function?

Answer:

Features of production function:

- The factors of production are substitute to each other

- Factors of production are supplementary to each other

- Some factors of production are specifie for specific goods.

Question 3.

Give the relationship between TP and MP?

Answer:

Relationship between TP and MP:

- When TP is maximum, MP is zero

- When TP increases at an increasing rate, MP is rising

- When TP rises at a diminishing rate MP is felling

![]()

Question 4.

What is the relationship between AP and MP?

Answer:

Relationship between AP and MP

- AP increases as a long as MP >AP AP is maximum and constant when MP = AP

- AP falls when MP = AP

- MP can be zero and negative but AP is never zero

Question 4.

Give the relationship between AP & TP?

Answer:

Relationship between AP and TP:

1, When TP increases at the increasing rate, AP increases.

2. When TP increases at a decreasing rate AP decreases.

3. TP and AP will always remain positive.

Question 5.

Give the relation between TP, AP and MP

Answer:

Relationship between TP, AP and MP

- In the intial stage TP AP and MP increase but MP is greater than AP

- When TP is maximum MP = o

- MP can be zero and negative but AP and are always positive.

- When AP is maximum and constant it is equal to MP

Question 6.

What do you mean by laws of returns? Give the types of laws of returns?

Answer:

Law of Returns:

Laws concerning the change in output due to change in inputs are known as the laws of returns. In other words, laws of returns explain the change in output as a result of a change in inputs They study how much change is brought about by the change in inputs.

Types of laws of returns:

There are two types of laws of returns:

- Laws of returns to a factor and

- Laws of returns to scale: Laws of returns to a factor are related to short period, whereas laws of returns to scale are related to long period

Question 7.

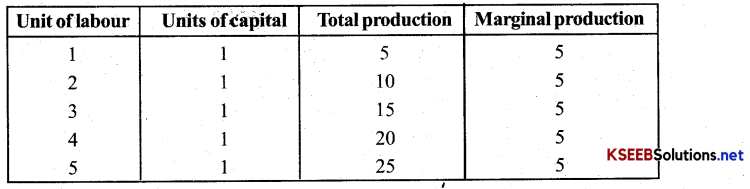

Make a table showing returns to a factor?

Answer:

Constant returns to a factor

From the table, we come to known that with the increase in the units of labour, total production increases at a constant rate and marginal production remains constant.

![]()

Question 8.

Write down three causes of constant returns to a factor?

Answer:

Cause of constant returns to a factor:

- Optimum utilization of the fixed factor We have the optimum utilization of fixed factors with ther increasing units of variable factor

- Most efficient utilisation of the variable factor: When more and more units ofthe variable factors are combined with the fixed factor, a stage comes when there is best possible division of labour, variable factor( a labour) is most effiecienty used. Accordingly, its marginal product remains to be constant at its maximum.

- Ideal factor ratio: With ihe increase in the unit of a factor, we get a stage where we have ideal factor ratio, It leads to constant returns to a factor

Question 9.

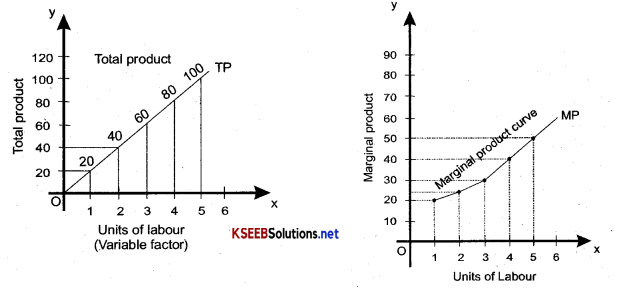

Draw TP and MP curves showing increasing returns to a factor?

Answer:

1. From diagram No. 1, we come to know that total production increases at the increasing rate with the increase in the units of labour( Variable factor)

2. From diagram No,2, we come to know that marginal product increases with the increase in the units of labour

Question 10.

Differentiate between internal and external economies?

Answer:

Internal Economics:

- These are the advantages which accure to a firm with expansion in its scale of production.

- These benefits are confined and specific to the individual firm arising from individual efforts

- Internal economies arise to large scale firms only

- Examples of internal economies are technical economies, Managerial economies marketing economies, risk-bearing economies.

External Economies

- These are the advantages which accure to a firm as a result of expansion of the industry as whole.

- These benefits are not Confind and specified to the individual firm.

- External economies are available to both large and small scale firm.

- Examples of external economies are the availability of transport facilities, commercial activities, services of banks etc.

Question 11.

What wre explicit and implicit costs? Give two examples of each?

Answer:

Explicit cost: Explicit cost are actually money costs which a firm ensures to make the payment to the hired factor of production According to Leftwich “ Explicit cost are those cash payment which firms make to outsiders for their servics and goods “ These costs include payments made to other and not to the owner himself for self – owned, self-supplied resources. Payment made to hired workers and payment made for raw materials Purchases are the example of explicit cost

Implicit cost:

These are estimated value of inputs supplied by the owner of the production unit. According to Leftwich , “Implicit costs of production are there costs of self – owned, self-employed resources that are frequently over looked in computing the expenses ofthe firms” Interest on the capital provided by the owner, the rent ofthe owners building used for the production units are the examples of implicit costs.

Question 12.

Explain the different between private costs and social costs?

Answer:

Private costs:

- These costs are incurred by an individual firm in producing commodity

- It is infact the money co st

- This cost has nothing to do with society

Social costs:

- These costs are disadvantages of producing a commodity suffered by the society as a whole.

- It does not take into consideration the money cost

- This cost is concerned with society.

Question 13.

Explain the difference between fixed costs and variable costs?

Answer:

Difference between fixed cost and variable cost:

| Fixed costs | Variable cost |

| 1. Fixed costs do not increase /decrease with the change in the level of output, i.e. they remain constant. | 1. Variable costs change with the change in the level of output, They increase/decrease with the increase /decrease in the level of output. |

| 2. They exist even at the zero levels of output. | 2. They do not exist at the zero levels of output. |

3. Fixed cost curve is parallel to OX axis |

3. Variable cost curve is positively sloping |

| 4. They remain constant | 4. They do not remain constant. |

| 5. A firm can continue produce even at the less of fixed costs | 5. Production is carried on only when variable costs are met. |

![]()

Question 14.

Explain the concept of opportunity cost with an example?

Answer:

Opportunity cost:

The concept of opportunity cost is the modem concept of cost. Opportunity cost of a factor refers to its value in its best alternative use. It is the opportunity cost or opportunity foregone in term of the next best alternative use of a factor.

According Prof. Leftwitch,” opportunity cost of a particular product is the value of the forgone alternative products that resources are used in its production could have produced” with reference to opportunity cost, two points must be kept in mind, First the opportuity cost of anything in the next best alternatives that could be Produced using the same amount of money, second the opportunity cost should be calculated on the basis of monetary value. The concept of opportunity cost can be explained with an example:- Suppose a farmes can grow wheat, gram and barley on a piece of land worth Rs.3400, Rs 2500 and Rs 2000 respectively. He grows wheat In this the oppurtunity cost will be Rs 1500 ( the next best alternative is growing gram worth Rs. 2500)

Long Answer Type Questions

Question 1.

Explain the laws of variable proportion Describe its three phases also

OR

What does the law of variable proportions show? State the behaviour of total product according to this law.

OR

What does the law of vaiable proportions show? state the behaviour of marginal product according to this law.

Answer:

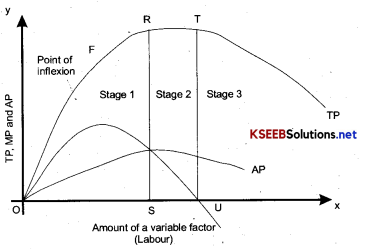

Laws of variable proportions. This law states that when the amount of variable factor is increased, given the quantity of other factors, average and marginal product first increase, then after reaching the maximum eventually diminish.

According to the law of variable proportions the production function with one variable factor has been divided into three stages. In stage I we have increasing returns to a factor, in stage 2 we have diminishing return to the factor and then in the stage III we have negative return to the factor. Thus, diminishing returns to a factor is only one phase or stage or the law of variable proportions.

Three stages of the law of vaiable proportion are shown in fig

First Stage: In first stage the total productiqn curve (TP) goes on increasing, first at increasing rate and then at a decreasing rate. The average product curve(AP) of the variable factor in stage I goes on increasing throughout. But marginal product curve of the variable factor rises for a long part in this stage in the beginning but a later part marginal product curve stats diminishing in stage I, but it still remains above about the average product.

Second Stage: In this stage total poduction is increasing all right , but it is increasing with diminishing rate till it reaches its maximum. The average production and marginal production are diminishing till marginal production becomes zero, where total production is maximum This stage is called the stage of law of diminishing marginal returns.

Third Stage: is the stage when total production starts diminishing,„ Marginal production is negative and average production is diminishing. How ever it should be noted that average production curve does not touch the X axis and it is not zero or negative.

Question 2.

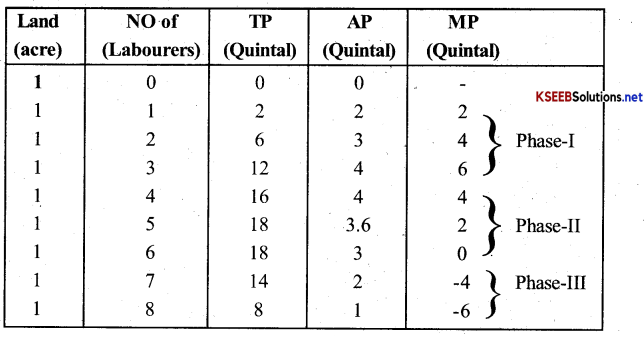

Explain the law of returns to a factor with the help of total product and marginal product schedule.

Answer:

Law of returns to a factor: The law states if more and more additional units of a variable factor are employed total physical Product (TPP) increases at increasing rate in the begining thert increase at diminishing rate and finally starts falling. It is a short period concept. It has three phases of production as shown in the schedule Here we have an assumed use oftwo factors in which land is the fixed factor and labour is a vaiable factor. The table shows succesive application of variable factor (labour) to the fixed factor of (land) to and the corresponding changes in output.

Phase-I: In this phase, TPP increase at an increasing rate MPP (marginal product) keeps rising. This phase is called phase of increasing returns.

Phase-II: In this phase, TPP increases at diminishing rate till it reaches its maximum output (18 in the table). MPP falls but remains positive It is called the phase of diminisghing returns to a factor. Out of three phases of production, this is crucial because a firm would always try to operate in this phase.

Phase-III: In this TPP starts declining, so phase III is called the phase of negative return . MPP becomes negative

![]()

Question 3.

Classify the following into fixed cost and variable costs. Give reasons.

(a) Rent for a shed

(b) Minimum telephone bill.

(c) Cost of raw material

(d) wages to payment staff

(e) Interest on capital

(f) Payment for transportation of goods

(g) Telephone charges beyond the minimum

(h) Daily wages.

Answer:

(a) Rent for a shed is fixed cost. It does not change with output.

(b) Minimum telephone bill is fixed cost because this payment has to made irrespective of the output produced.

(c) Cost ofraw material is a variable cost as it increases or decreases with the change in the level of output produced.

(d) Wages to permanent staff is a fixed cost as permanent staff will have to be paid | salary whatever may be the output level being produced by the firm.

(e) Interest on fixed capital is a fixed cost because the firm owner has borrowed & invested the sum & now, what ever may be the level of output produced interest on borrowed sum, will have to be paid.

(f) Payment for transportation of goods is vaiable cost, because if the output increases, more would have to be spent on the transportation of this higher output,

(g) Telephone charges beyond the minimum a variable cost as frequency of telephone calls is expected to increase with output.

(h) Daily wages is variable cost because for producing a higher output, one will have to employ more working on daily wages & hence this payment would increase with I output.

Question 4.

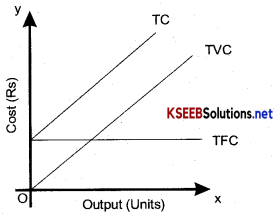

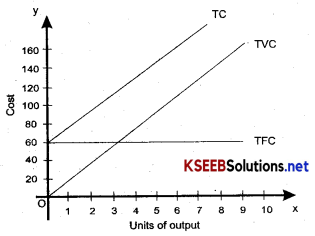

What are the total fixed, total variable cost & total cost of a firm? How are they related?

Answer:

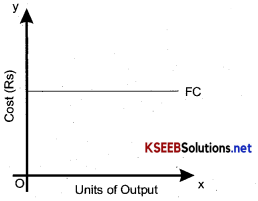

Total fixed cost: It refers to that cost that remains constant (unchanged) at different levels of output.

Hence total fixed cost curve is a straight line parallel to the output axis.

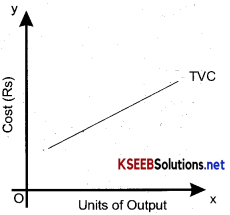

Total variable cost: It is the difference between the total cost & variable cost = (TVC = TC – TC)

It increases with the increase in the level of output. It is influenced by the law of proportion.

Total cost: It is the sum total of total fixed cost & total variable cost

Total cost = TFC + TVC

Relationship between total fixed cost, total variable cost & total cost of a firm.

As the input increases total variable cost & hence total cost increases. The total fixed cost, however, is independent of the amount of output produced & remain constant for all levels of production.

At the zero level of output, total cost is equal to total fixed cost.

Question 5.

Explain the meaning of various short-run costs?

Answer:

Total fixed cost( TFC): Total fixed cost is payment for fixed factors in the short run. It does not change with the change in the level of production.

Total variable cost(TVC): Total variable cost includes payment made to the variable factors of production. It changes alohg with the quantity of output.

Total cost (TC): Total cost includes both total variable cost & total fixed cost

Average fixed cost (AFC): It is the per unit fixed cost of production cost a commodity. We can obtain average fixed cost by dividing the total fixed cost by the number of unit produced.

Average variable cost( AVC): Average variable cost is the per unit variable cost of production of a commodity we obtain average variable cost by dividing the total variable cost by the number of unit produced.

Average cost(AC): Average cost is the per-unit total cost of production. We can obtain the average cost by dividing the total cost by the number of unit produced.

Marginal cost: Marginal cost is the cost of producing an extra unit of commodity.

Exercises

Question 1.

Explain the concept of a production function?

Answer:

Production function, explains the relationship between factor input & output under given technology.

OR

According to Watson” production function is the relationship between physical inputs and physical output of a firm”

In symbolically:

Y = f(R, L, K, O….)

Where y = output

R= Land

L= Labour

K= Capital

O = Organisation

Question 2.

What is the total product of an input?

Answer:

Total product indicates the total volume of goods and service produced during a specified period of time generally a year.

In short, it is the sum of marginal products, It is also called total physical product

TP = ΣMP

Where, TP= Total product

Σ MP = sum of marginal product

![]()

Question 3.

What is the average product of an input?

Answer:

Average product is defined as the out put per unit of variable input. We calculate it as

OR

AP1 = \(\frac{\mathrm{TP}}{\mathrm{X}_{1}}=\mathrm{f} \frac{\left(\mathrm{x}_{1}: \overline{\left.\mathrm{x}_{2}\right)}\right.}{\mathrm{x}_{1}}\)

OR

AP1 = \(\frac{\text { Total Product }}{\text { No. of unit of a variable factor }}\)

OR

\(\frac{\mathrm{TP}}{\mathrm{L}}\)

Question 4.

What is the marginal product of an output?

Answer:

Marginal product is defined as the increase in output due to increase in one extra unit of the variable input to the production process when all other factor input are held constant.

Question 5.

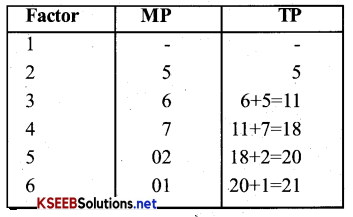

Explain the relationship between the marginal product and the total product of an output?

Answer:

The relationship between the marginal product and total product of an output.

There is a close relationship between the marginal product and total product of an input. For any level of employment of factor input, if we add up the marginal product for every unit of the factor upto that level, we get the total product of that factor at that level of employment.

The relationship between MP and TP has shown with the help of the following table:

Question 6.

Explain the concepts of the shortrun and longrun?

Answer:

In microeconomics, the longrun is the conceptual time period in which there are no fixed factors of production, so that there are no constraints preventing changing the output level by changing the capital stock or entering or leaving an industry.

The shortrun, in which some factors are variable and others are fixed, constraining entry or exit from an Industry,

In the long run, firms change production level in response to economic profits or losses and the land, labour, capital goods and enterpreneurship vary to reach the minimum level of long- run average cost.

Where as in short run all production in real occurs. In the shortrun, a profit maximizing firm will:

- Increase production if MC is lesser than marginal revenue.

- Decrease production if MC is greater than MR.

- Continuing producing if average variable cost is less than price per unit even if average total cost is greater than price.

- Shut down if average variable cost is greater than price, at each of outputs.

Question 7.

What is the law of diminishing marginal product?

Answer:

Law of diminishing marginal product states that if we increase the amount of variable input, the marginal product of that, input after a certain level of employment starts falling.

Question 8.

What is the law of variable proportions?

Answer:

The law of variable proportion explains the relationship between the proportion of first input and variable input on the one hand and output on the other.

Question 9.

When does a production function satisfy constant return to scale?

Answer:

Production friction satisfies constant return fo scale when proportional increase in all inputs result in an increase in input by the same proportion.

![]()

Question 10.

When does a production function satisfy increasing returns to scale?

Answer:

A production function satisfies increasing return to scale when a proportional increase in all input return in an increase in output by more than the proportion.

Question 11.

When does a production function satisfy decreasing return to scale?

Answer:

A production function satisfies decreasing returns to scale when a proportional increase in all inputs results in an increase in output by less than the proportion,

Question 12.

Briefly explain the concept of the cost function?

Answer:

Concept of the cost function:

In order to produce output the firm needs to employ input. The firm as to increase some expenses for employing the input. These expenses are known as cost The output-cost relationship is the cost function of the firm These can be led by several different input combinations with which a firm can produce a desired level of output. with the input price given, the firm will choose that combination of input which is least expensive. So for every level of output the firm choose the least-cost input combination.

Question 13.

What are the total fixed cost, total variable cost and total cost of a firm? and how are they related?

Answer:

Total Fixed cost:

Fixed cost is payment made for fixed factors in the short run . It does not change with the change in the level of production.

Total variable cost:

Variable cost includes payment made for the variable factors of production. It changes along with the quantity of output.

Total cost:

It is the total expenditure on the factors and non- factor input in the production of goods& services.

The relationship between TFC,TVC, & TC:-

Total cost includes both total variable cost & total fixed cost, total cost can be written as

TC = TFC + TVC.

Total cost is illustrated in diagram below.

In the diagram, unit of output is measured on OX Axis & the cost on OY Axis, It is clear that TFC of a firm remain same at various levels of output , There is TFC even when the production is Zero. TVC increases with increase in the level of output. It starts from the origin and increases slowly upto the third unit of output. It begins to increase at an increasing rate. Afterwards the TC, which is the sum of TFC and TVC increases with increase in the level of output, There is TC even when production is Zero.

Question 14.

What are the average fixed cost , average variable cost & average cost of a firm? How they are related?

Answer:

Average fixed cost (AFC):

It is per unit fixed cost of production of a commodity. We can obtain average fixed cost by deciding the total fixed cost by the number of unit produced.

Formula:

AFC = \(=\frac{\text { Total Fixed Cost }}{\text { No. of units produced }}\)

OR

AFC = \(\frac{\mathrm{TFC}}{\mathrm{Q}}\)

OR

AFC = \(\frac{\mathrm{TFC}}{\text { Units }}\)

Average variable cost(AVC):

Average variable cost is the per unit variable cost of production of a commodity. We can obtain average variable cost by dividing the total variable cost by the number of units produced

Formula:

AVC = \(\frac{\text { Total variable cost }}{\text { No. of unit produced }}\)

OR

AVC = \(\frac{\mathrm{TVC}}{\mathrm{Q}}\)

OR

AVC = \(\frac{\text { TVC }}{\text { Units }}\)

Average cost(AC):

The average cost is the per-unit total cost of production. We can obtain the average cost by dividing the total cost by the number of units produced.

Formula:

AC = \(\frac{\text { Total cost }}{\text { No. of unit produced }}\)

OR

AC = \(\frac{\mathrm{TC}}{\mathrm{Q}}\)

OR

AC = \(\frac{\text { TC }}{\text { Units }}\)

Relationship between AFC, AVC & AC

- AC = AFC + AVC

- AFC = AC – AVC

- AVC = AC – AFC

Question 15.

Can there be some fixed cost in the long run? If not, why?

Answer:

No, there cannot be any fixed cost in the long run because in the long run that there will be no fixed inputs.

Question 16.

What does the average fixed cost curve look like? Why does it look so?

Answer:

The average fixed cost cruve looks like a rectangular hyperbola. It approches zero but it never become zero . It always remain positive. It is rectangular hyperbola because it shows that the area under the curve (i,e. Total fixed cost) always remain same.

![]()

Question 17.

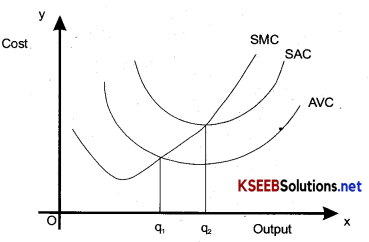

What do the short-run marginal cost, average variable cost, & short-run average cost curve look like?

Answer:

Shortrun marginal average variable cost and short-run cost look like “U” shape. It is due to : Law of variable proportions” it may be shown as under.

Question 18.

Why Does the SMC curve cut the AV C curve at the minimum point of AVC curve?

Answer:

As long as AVC is falling, SMC must be less than the AVC and as AVC rises, SMC must be greater than the AVC. So the SMC curve cuts the AVC curve from below at the minimum point of AVC.

Question 19.

At which point does the SMC curve cut the SAC curve? Give a reason in support of your answer?

Answer:

Similar to the case of AVC & SMC, here too as long as SAC is feeling SMC is less than the SAC and when SAC is rising, SMC is greater than the SAC. SMC curve cuts the SAC curve from below at the minimum point ofSAC.

Question 20.

Why is the short run marginal cost curve ‘U’- shaped?

Answer:

Shortrun marginal cost curve is U- shaped due to operation law of variable proportions. Marginal cost fells in the beginning, than remain constant and ultimately rises. Falling marginal cost is in accordance with rising MP, when these are increasing returns to a factor risinfg MC is in accordance with falling MP when there are diminishing return to a factor.

Question 21.

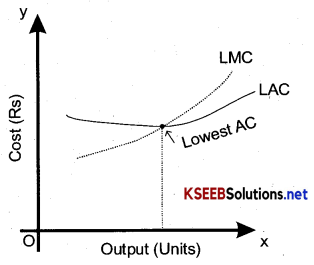

What do the long run marginal cost and the average cost curve look like?

Answer:

Long run marginal cost and the average cost curve are U- shaped, but they are flatter as shown below:-

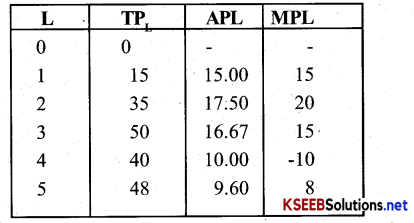

Question 22.

The following table gives the total product schedule of labour, find the corresponding average product and marginal products schedules of labour.

| L | IPL |

| 0 | 0 |

| 1 | 15 |

| 2 | 35 |

| 3 | 50 |

| 4 | 40 |

| 5 | 48 |

Answer:

Question 23.

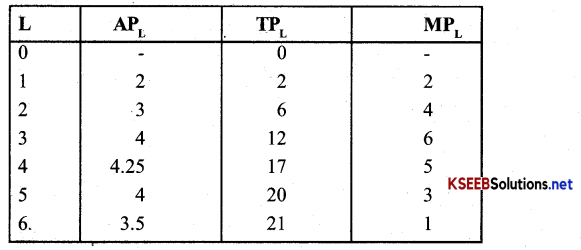

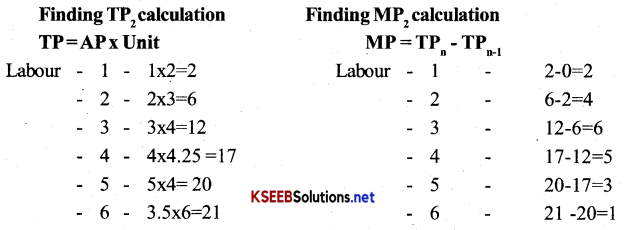

The following table gives the average product schedule of labour. Find the total product and marginal product schedules. It is given that the total product is zero level of labour employment.

| L | APL |

| 1 | 2 |

| 2 | 3 |

| 3 | 4 |

| 4 | 4.25 |

| 5 | 4 |

| 6 | 3.5 |

Answer:

![]()

Question 24.

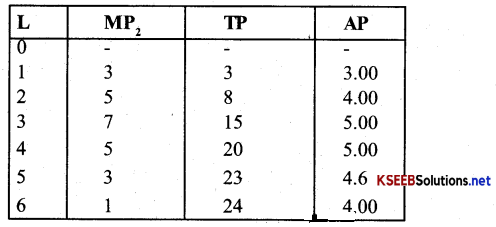

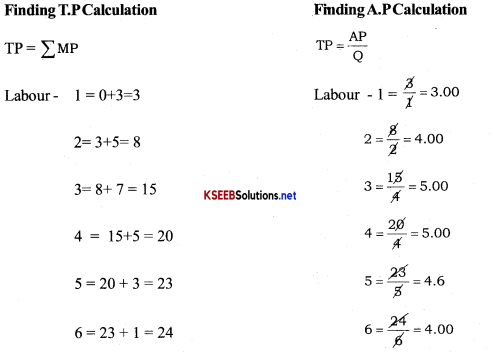

The following table gives the marginal product schedule of labour, It is also given that total product of labour is zero at zero level of employment, Calculate the total and average product schedules of labour.

| L | MPL |

| 1 | 3 |

| 2 | 5 |

| 3 | 7 |

| 4 | 5 |

| 5 | 3 |

| 6 | 1 |

Answer:

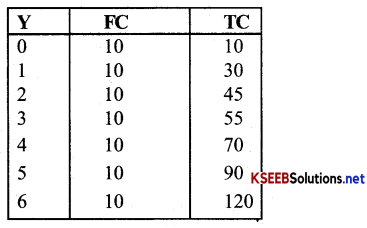

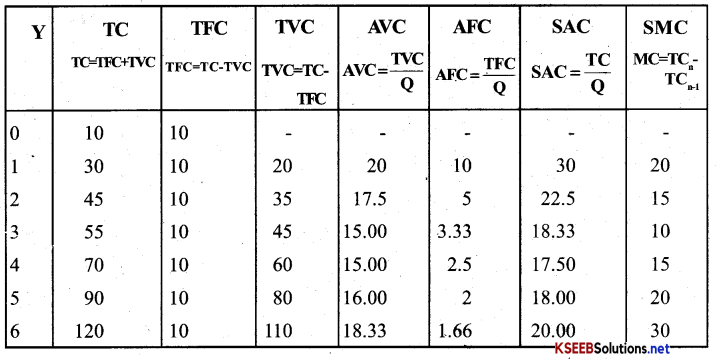

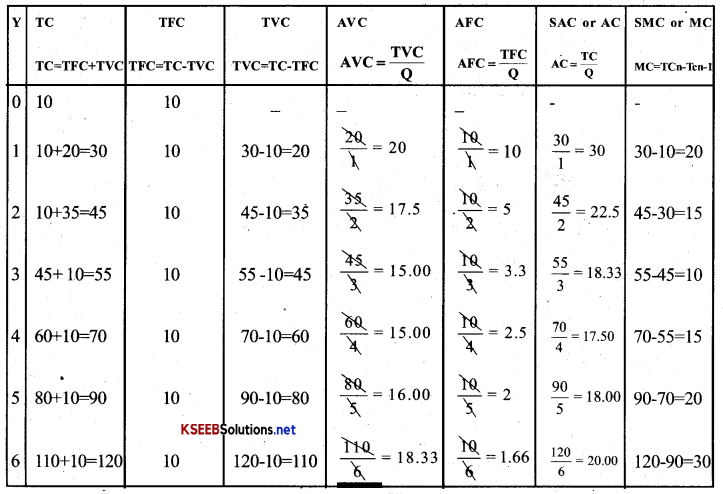

Question 25.

The following table shows the total cost schedule of a firm. What is the fixed cost schedule of this firm? Calculate TVC, AFC, AV C, SAC & SMC schedules of the firm?

| Y | TC |

| 0 | 10 |

| 1 | 30 |

| 2 | 45 |

| 3 | 55 |

| 4 | 70 |

| 5 | 90 |

| 6 | 120 |

Answer:

Total fixed cost schedule of a firms:

At zero level of input, TC = FC. In the table, TC at zero level of output is 10 Hence, FC will be 10. The fixed cost remains constant. So the fixed cost will be 10 at level of output

Finding of all costs:

Calculation:

∴ In such way the simple calculations can be done easily with the help of formula’s.

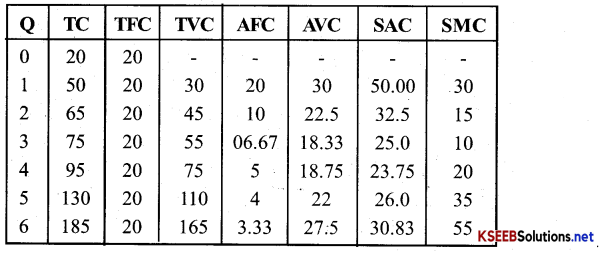

Question 26.

The following table gives the total cost schedule of a firni It is also given that the average fixed cost at 4 units of output is Rs 5, Find the TVC,TFC, AVC, AFC,SAC and SMC schedules of the firm for the corresponding value of output.

Answer :

Here AFC at 4 unit of output is Rs5, with this information, we will calculate TFC by multiplying 4 × 5, TFC will be Rs 20, at all levels of output TFC will be 20 and TC will also 20 at zero lead of output ;

Question 27.

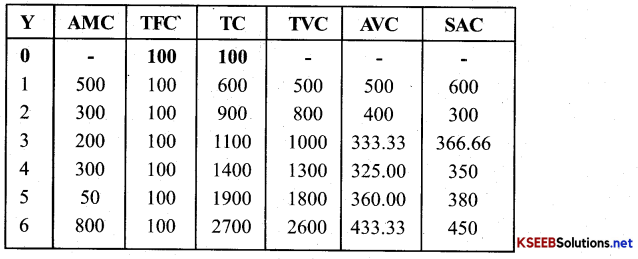

A firm’s SMC schedules is shown in the following table; The total fixed cost of the firm is RslOO. Find TVC, TC, AVC, and SAC schedules of the firm.

Answer:

Question 28.

Let the production function of a firm be: Q = 5L1/2 k1/2. Find out the maximum possible output that the firm can produce with 100 units of L and 100 of K

Answer:

Q = 5L1/2 k1/2

OR maximum output

= 5 × 1001/2 × 1001/2.

= 5 × 10 × 10 = 50 × 10 = 500

![]()

Question 29.

Let the production function of a firm be Q = 2L2 K2. Find out the maximum possible output that the firm can produce with 5 units of L and 2 units of K, What is the maximum possible output that the firm can produce with zero unit of L and 10units of K?

Answer:

1. Q = 2L2K2

OR output = 2 × 52 × 22

= 2 × 25 × 4

= 200 units

2. The maximum output would be zero with zero unit of L and 10 unit of K. The reason is that the production function, our assumption is that if any out put becomes zero, then the production would also be zero. Since here labour is zero, the out put would also be zero

Question 30.

Find out the maximum possible output for a firm with zero unit of L and K when its producion function is Q = 5L + 2K

Answer:

In production function, our assumption is that if any input becomes zero the production would also be zero. Since here labour is zero, the out put would also be zero.